I once needed to move R50,000 from a UK prop firm payout back to South Africa.

David van der Merwe

Emerging Markets Trader ·  South Africa

South Africa

☕ 10 min read

What you'll learn:

- 1What FNB Forex Branches Actually Do (And Don't Do)

- 2The Real Costs: Fees, Spreads, and The Hidden Tax

- 3SARB's Rules: The Invisible Cage for Your Capital

- 4FNB Forex vs. Retail Forex Brokers: A Trader's Comparison

- 5The Right Way: Funding a Trading Account from SA

- 6Common (and Costly) Trader Mistakes with Bank Forex

- 7When You *Should* Actually Use an FNB Forex Branch

- 8The Future: The COFI Bill and What It Means for You

I once needed to move R50,000 from a UK prop firm payout back to South Africa. Thinking my local FNB forex branch in Sandton was the 'safe' option, I walked in. The teller quoted me a rate that was 3.2% worse than the interbank rate I saw on my trading platform. After their R200 fee, I was down over R1,600 before the money even landed. That loss, on a simple transfer, taught me the brutal difference between a bank's forex service and a trader's forex market. This guide isn't about finding an FNB branch (there are plenty). It's about understanding what they really offer and why, as a trader, you should almost never use them for your actual trading.

Let's be clear from the start. An FNB forex branch is not a retail trading desk. You cannot walk into one in Rosebank or Sandton City, open a MetaTrader terminal, and start scalping the EUR/USD. Their primary function is facilitating international transfers, selling physical foreign cash (notes), and helping clients with structured foreign exchange needs under South African Reserve Bank (SARB) regulations.

Their customers are typically businesses making supplier payments, individuals sending money to family abroad, or travelers buying holiday cash. The pricing is built for these large, infrequent transactions where convenience and compliance trump cost-efficiency. The spread - the difference between the buy and sell price - is where they make their money, and it's hefty.

Warning: Using a bank for active trading execution is like using a cargo ship for a speedboat race. The infrastructure, costs, and purpose are fundamentally mismatched. For the mechanics of a real trading instrument, see our EUR/USD guide.

I learned this the hard way. After my expensive transfer, I asked about their rates for frequent small transactions. The banker looked confused and just pointed back to the fee schedule. Banks are not built for the frequency or precision required in trading.

This is where the rubber meets the road. FNB's fees are structured for occasional use, which makes them prohibitively expensive for trading. Let's break down the two main costs.

The Stated Fees

Based on their latest schedules, sending money internationally costs a flat fee plus a percentage. For an online transfer over R10,000, you'll pay 0.55% (min R275, max R550). Need phone or banker assistance? That minimum jumps to R550. Receiving money from overseas also incurs a fee of 0.55% for amounts over R10,000.

These are just the ticket charges. The real killer is the spread.

The Spread: Your Silent Partner in Loss

FNB applies an exchange rate margin, typically between 1% and 4%. Let's do the math with a real example from a client statement I reviewed.

Example: A client wanted to convert R100,000 to USD for an investment. The interbank mid-rate was 18.50 ZAR/USD. FNB's offered rate was 19.02 ZAR/USD. That's a 2.8% margin.

- At Interbank Rate: R100,000 / 18.50 = $5,405.41

- At FNB's Rate: R100,000 / 19.02 = $5,257.62

- Hidden Cost: $147.79 (or about R2,735) lost to the spread. Add the R550 transfer fee, and the total cost to access those dollars was over R3,285. That's a 3.3% haircut before your money even leaves the country. In trading, where professional brokers offer spreads as low as 0.0 pips on majors, a 3% cost would obliterate any strategy. This is why understanding the spread definition is foundational.

💡 Winston's Tip

Your bank's forex desk is a toll booth, not a trading floor. Pay the toll when you must move money, but never try to trade there. The toll fee is 100 times the market rate.

“Using a bank for active trading execution is like using a cargo ship for a speedboat race.”

Every transaction at an FNB forex branch operates within a strict cage built by the South African Reserve Bank (SARB). Ignoring these rules isn't an option; they will block your transaction. As a trader, you must know these limits cold.

You have two key annual allowances:

- Single Discretionary Allowance: R1 million per calendar year. No tax clearance needed. Use it for travel, gifts, online subscriptions.

- Foreign Investment Allowance: R10 million per calendar year. This requires a Tax Compliance Status (TCS) pin from SARS. This is what you'd use for funding an international brokerage account.

Pro Tip: Apply for your TCS pin from SARS before you need it. The process can take weeks. Having it ready means you can move funds quickly when a trading opportunity arises, without waiting on bureaucracy.

A critical rule: if you don't use your travel allowance (say, you bought USD but didn't travel), you must sell the foreign currency back to an authorized dealer like FNB within 30 days of your intended return date. Failure to do this can lead to penalties and affect future allowances.

For amounts over R1 million, you'll need an Approval of International Transfer (AIT) from SARS. They'll want proof of source of funds - this is where your trading statements from a reputable broker like Pepperstone or IC Markets become crucial documentation.

This is the core of the argument. Choosing between an FNB branch and a broker isn't about preference; it's about choosing the right tool for the job. One is for moving money, the other is for making money from price movement.

| Feature | FNB Forex Branch | International Retail Broker (e.g., Exness, XM) |

|---|---|---|

| Primary Purpose | International Transfers, Compliance | Speculative Trading, Investment |

| Typical Spread on EUR/USD | 1-4% (200-400 pips) | 0.1-1.0 pips (0.001-0.01%) |

| Transaction Cost | High Fees + Wide Spread | Tight Spread + Low/No Commission |

| Trading Platform | None for speculation | MetaTrader 4/5, cTrader, Proprietary |

| use | Not Offered | Up to 1:500 (or more, depending on regulator) |

| Speed of Execution | Days for transfers | Milliseconds for trades |

| SARB Allowance Used | Discretionary or Investment | Investment Allowance (with TCS) |

Think of it this way: if you need to pay for a course in the US, use FNB. If you want to trade your view on the US dollar, you must use a broker. The cost differential alone makes bank forex suicidal for active trading. A single 2% spread at FNB wipes out the average monthly return of a good swing trading strategy.

💡 Winston's Tip

Get your SARS Tax Compliance Status pin now, while you don't need it. When a market opportunity arises, you'll be ready to fund your account in days, not weeks. Bureaucracy is the slowest moving average of all.

“The spread at a bank isn't a fee; it's a silent partner that takes its cut before you even see the price.”

So, you've opened an account with a global broker. How do you get your ZAR to them legally and cost-effectively? FNB can be a part of this process, but only as the sending bank, not the trading venue.

Here's the step-by-step I use and recommend to my clients:

- Choose Your Broker: Ensure they accept international clients and support ZAR wire transfers. Most major brokers like Pepperstone do.

- Get Your Tax Compliance Status (TCS): Log onto SARS eFiling and apply for a TCS pin for 'Foreign Investment'. This is non-negotiable for using your R10 million allowance.

- Initiate a SWIFT Transfer via FNB: Use FNB's online banking or visit a branch. You will need:

- The broker's banking details (account name, number, SWIFT/BIC).

- Your TCS reference.

- The purpose: "Investment in offshore brokerage account."

- Track and Confirm: SWIFT transfers take 2-5 business days. The broker will convert your ZAR to your trading account currency (usually USD, EUR) at a near-interbank rate.

Warning: Never try to use multiple small transfers under the R1 million discretionary allowance to fund trading. This is a red flag for SARS and SARB's Financial Surveillance Department. It's called 'smurfing' and can get your entire financial profile flagged. Use the proper investment channel.

The total cost? The FNB transfer fee (0.55%, max R550) plus the broker's tiny conversion spread. Far cheaper than trying to trade through the bank.

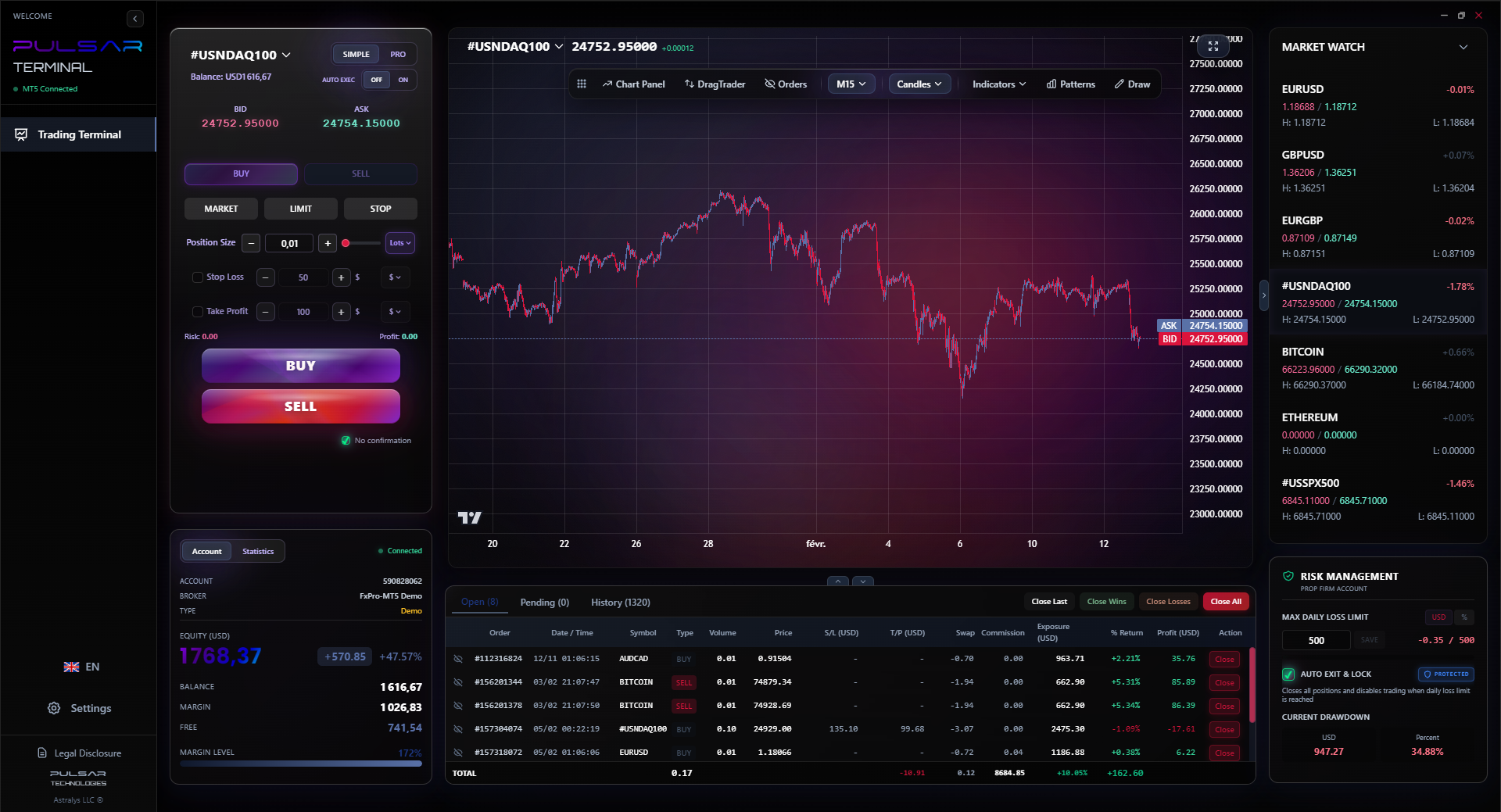

Once your capital is with a proper broker, managing risk with precise tools becomes critical; Pulsar Terminal's drag-and-drop order system and multi-TP/SL features let you execute complex trade plans on MT5 faster than a bank teller can quote you a rate.

Pulsar Terminal

The all-in-one MT5 companion: drag-and-drop orders, multi-TP/SL, trailing stop, grid trading, Volume Profile, and prop firm protection. Used by 1,000+ traders daily.

I've seen every variation of these errors. They all stem from not understanding the fundamental difference between a banking product and a trading market.

Mistake 1: Using a Travel Card for 'Trading' Trips. Some think loading an FNB Travel Card with USD is a hedge for a trading trip. It's not. You're locking in a terrible rate upfront. If the ZAR strengthens while you're away, you lose. It's a static, costly position. Better to use a global debit card linked to your ZAR account and let the real-time Visa/Mastercard rate handle it - it's always better.

Mistake 2: Trying to 'Hold' Currency in a Bank Account. Opening an FNB Foreign Currency Account to 'hold' USD while you wait for a trade idea is a losing game. You pay the wide spread to buy, and you'll pay it again to sell. You're making two terrible 'trades' with the bank. A trading account with a broker holds the currency for you at spot, with no spread penalty for entering and exiting.

Mistake 3: Not Factoring in the Full Cost. Traders look at the R550 fee and think, 'That's fine for a R100k transfer.' They ignore the 3% spread loss, which is 5-6 times larger. This blindness to total cost is what blows up retail accounts. Always use a position size calculator that includes the true cost of trade entry, which for a bank would be astronomical.

My own mistake was arrogance. I thought because I could read a MACD indicator on a chart, I understood currency markets. I didn't understand the institutional market structure that sits between a retail bank and the interbank system. That gap is where your profit goes to die.

“FNB for logistics, brokers for execution. Confuse the two and you'll subsidize the bank's profits with your trading capital.”

It's not all bad. There are specific, limited cases where walking into an FNB forex branch in Johannesburg makes perfect sense.

- You Need Physical Foreign Cash Tomorrow: Flying to Kenya and need KES? An FNB branch in Sandton or Rosebank can often provide it same-day or next-day, which is faster than most currency exchanges. Just know you're paying a premium for that convenience.

- You Have a Large, Legitimate International Payment: Paying for a property deposit in the UK, or settling a large invoice for a business. The bank's compliance team and structured process are assets here, not liabilities. The cost is just a line item in a large transaction.

- You Need Help with SARB Compliance Paperwork: If your TCS application is stuck or you're confused about the AIT form, a banker at a major branch can sometimes provide guidance. They see these forms every day.

- Repatriating Trading Profits: This is the virtuous cycle. When you withdraw profits from your IC Markets account back to your FNB account, you'll use the SWIFT network. The bank receives the USD, converts it to ZAR (yes, with their spread), and deposits it. Here, the spread is a cost of doing business - a tax on success. It hurts, but it's coming out of profits, not capital.

In essence, use them for logistics and compliance, not for execution or speculation.

💡 Winston's Tip

If your trading strategy can't survive a 3% transaction cost, it's not a strategy. It's a hope. FNB's spread is the ultimate stress test for your edge.

The regulatory ground is shifting. The Financial Sector Conduct Authority (FSCA) is working on the Conduct of Financial Institutions (COFI) Bill, aiming for finality in the 2026 fiscal year.

This won't directly change FNB's spreads. But it aims to create an 'outcomes-based' framework. In plain English, this could mean more scrutiny on whether banks are treating customers fairly when providing forex services. Are they explaining that 3% spread clearly? Is the pricing transparent?

For you, the trader, the greater impact may be on the broker side. COFI could lead to stricter oversight of the marketing and sign-up practices of international brokers targeting South Africans. The goal is to reduce 'customer harm' from misunderstood leveraged products. This makes choosing a well-regulated, transparent broker even more critical.

The lesson is that regulation is a constant. Whether it's SARB's exchange controls or the FSCA's conduct rules, operating in the South African financial space means playing within a strict set of rules. The smart trader learns the rules, uses the right tools for each task (FNB for transfers, brokers for trading), and always, always calculates the true cost. Your edge depends on it.

FAQ

Q1Can I trade forex at an FNB branch in Johannesburg?

No. FNB forex branches do not offer speculative trading platforms like MetaTrader. They provide currency exchange and international transfer services. For active trading, you must use a licensed retail forex broker.

Q2What is the cheapest way to send money overseas from South Africa?

For large amounts (like funding a trading account), a SWIFT transfer using your R10 million foreign investment allowance is the standard method. While FNB charges a fee (0.55%, max R550), the overall cost is lower than using their spot rate for conversion. For smaller amounts, specialized international money transfer services often offer better rates than banks.

Q3How much can I send overseas without tax clearance?

You can use your Single Discretionary Allowance of R1 million per calendar year without a Tax Compliance Status (TCS) pin from SARS. For any amount from R1 to R10 million, you must use your Foreign Investment Allowance, which requires a TCS pin.

Q4Why is FNB's exchange rate worse than the rate on Google?

The rate on Google is a mid-market 'interbank' rate, the theoretical average between the buy and sell price in the wholesale market. FNB adds a margin (1-4%) to this rate to create their sell price to you. This spread, not just the fee, is their primary revenue from the transaction.

Q5Is it legal to use international forex brokers as a South African?

Yes, it is legal. You must use your Foreign Investment Allowance (with SARS tax clearance) to fund the account and declare any offshore investments on your tax return. The broker must also be licensed by a reputable foreign regulator like the FCA, ASIC, or CySEC.

Q6What happens if I don't use my travel allowance and keep the foreign cash?

You are required by SARB regulations to resell any unused foreign currency from a travel allowance to an authorised dealer (like FNB) within 30 days of your return to South Africa. Failure to do so can result in penalties and may affect your future access to foreign allowances.

Q7Can I open a US Dollar account with FNB to hold trading funds?

Yes, FNB offers Foreign Currency Accounts. However, this is inefficient for trading. You pay FNB's wide spread to fund it and again to empty it. It's better to send funds directly to your international broker, where the currency is held at spot value and can be traded with tight spreads.

Prof. Winston's Lesson

Key Takeaways:

- ✓Bank forex spreads (1-4%) are 100x wider than broker spreads.

- ✓Use SARB's R10m investment allowance, not the travel allowance, for trading.

- ✓Always get your SARS TCS pin before you need to fund an account.

- ✓The true cost is the fee PLUS the spread. Most only see the fee.

How useful was this article?

Click a star to rate

Weekly Trading Insights

Free weekly analysis & strategies. No spam.

About the Author

David van der Merwe

Emerging Markets Trader

Johannesburg-based trader with 11 years in emerging market currencies. Specializes in ZAR pairs, FSCA-regulated trading, and South African market analysis.

Comments

Risk Disclaimer

Trading financial instruments carries significant risk and may not be suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always conduct your own research before trading.

You Might Also Like

Cara Trading Forex Sukses: 7 Prinsip dari Trader Profesional

Cara trading forex sukses dengan 7 prinsip trader pro: manajemen modal, disiplin, journal trading, backtest. Data nyata, bukan janji profit palsu.

Jam Trading Forex Terbaik untuk Trader Indonesia: Panduan Lengkap dengan Tabel Waktu

Panduan jam trading forex untuk trader Indonesia. Tabel 4 sesi dunia, jam emas 20:00-00:00, sesi mana yang harus dihindari. Data akurat + tips dari trader berpengalaman.

Top 5 Sàn Forex Uy Tín Nhất 2026: Review Jujur dari Trader Indonesia

Top 5 sàn forex uy tín 2026 untuk trader Indonesia. Review jujur: spread, deposit, withdraw, dukungan lokal. Exness, XM, IC Markets & lebih.

Get Pulsar Terminal

All these calculators are built into Pulsar Terminal with real-time data from your MT5 account. One-click position sizing, automatic risk management, and instant calculations.

Get Pulsar Terminal