Liquidity

lih-KWID-uh-teesince Early 20th century financial marketsLiquidity — how easily you can get in and out of trades without causing price ripples - basically the market's 'thickness' or 'thinness'.

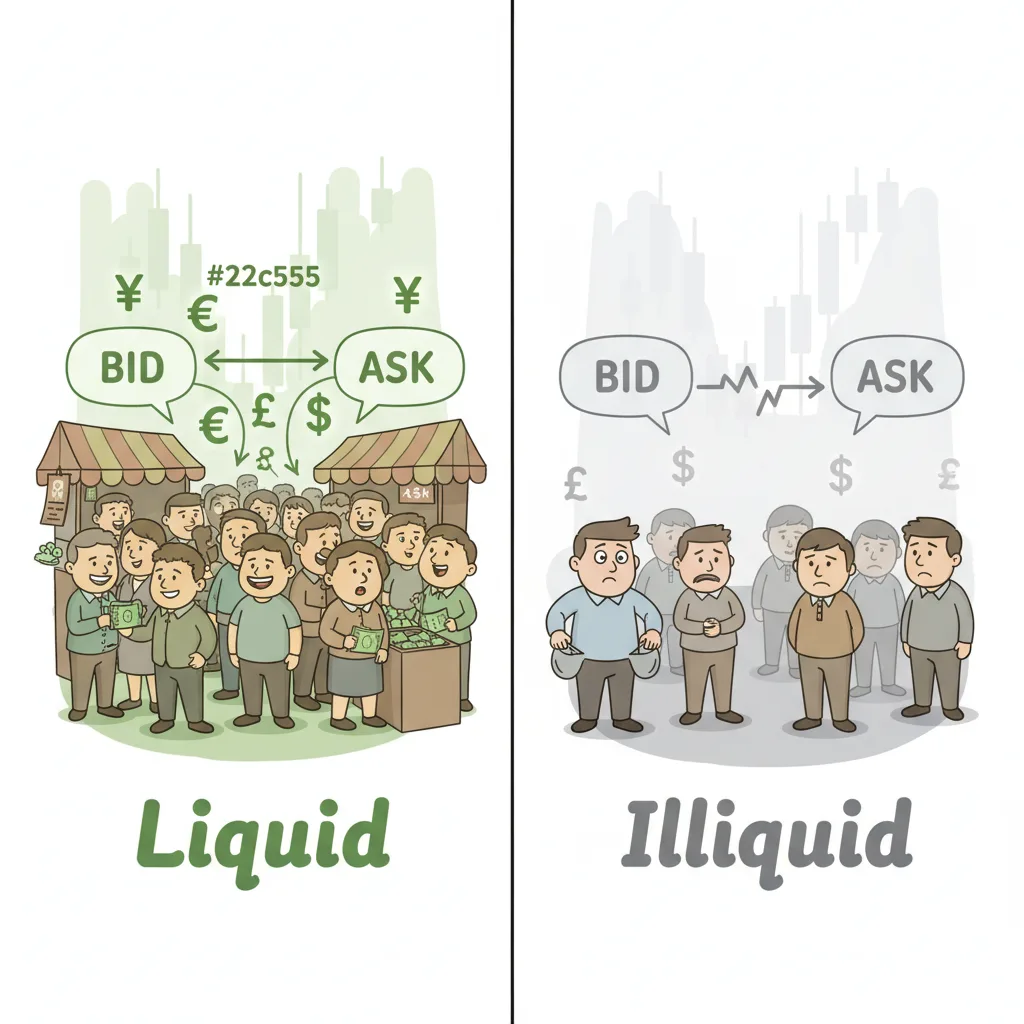

§1So, what IS liquidity anyway?

Okay, picture this: you're at a packed farmers market on Saturday morning. You want to sell your homemade jam. There are dozens of people milling about, some looking for jam, others selling different goods. You shout 'Fresh strawberry jam for $5!' and boom - three people immediately want it. That's high liquidity, my friend. Now imagine that same market at 3 AM on a Tuesday. You're standing there with your jam, crickets chirping, maybe one sleepy security guard walks by. That's low liquidity. In trading terms, liquidity is all about how easily you can buy or sell something without causing a scene. When there are tons of buyers and sellers (like EUR/USD during the London-New York overlap), you can slip in and out of trades like a ninja. When it's thin (like some exotic pairs during off-hours), your trades make waves. I've seen traders blow accounts because they didn't respect liquidity - trying to move big money in thin markets is like trying to turn a cruise ship in a bathtub.

§2The numbers behind the magic

Don't worry, we're not doing calculus here. The main way we measure liquidity is through the bid-ask spread. Think of it as the 'cover charge' to enter the market club. Absolute Spread = Ask Price - Bid Price. Simple, right? If EUR/USD is quoted at 1.08000 bid and 1.08001 ask, that's a 0.1 pip spread - basically the market saying 'Come on in, the water's fine!' But if USD/TRY is at 32.4500 bid and 32.4550 ask, that's a 5-pip spread - more like 'Entry fee: one kidney.' We also look at percentage spreads to compare different priced assets, and turnover ratios to see how often things change hands. The key takeaway? Narrow spread = high liquidity = happy trader. Wide spread = low liquidity = proceed with caution.

§3Here's how it plays out in your trades

Let's walk through two real scenarios. First, high liquidity: It's peak trading time, and EUR/USD is buzzing at 1.08000/1.08001. You want to buy 1 standard lot. Click - executed instantly at 1.08001. No drama, no fuss. Price moves to 1.08100? You've made 9.9 pips profit. Now, low liquidity: It's 3 AM your time, and you're trading USD/TRY at 32.4500/32.4550. You try to sell 1 lot. Instead of getting 32.4500, you might slip to 32.4450 because there just aren't enough buyers lined up. That's slippage - liquidity's annoying cousin. If price then drops to 32.4000, your profit starts from that worse entry. See how liquidity directly hits your bottom line?

§4The weird stuff nobody warns you about

Oh, markets love exceptions. First, news events - think Non-Farm Payrolls Friday. Suddenly, spreads that were 1 pip can balloon to 20+ pips. It's like the market collectively holds its breath, then screams. Second, offshore brokers vs regulated ones. In the EU, leverage for majors is capped at 30:1. Offshore? They might offer 500:1 or even 1000:1. Sounds great until you realize thin liquidity plus crazy leverage equals account explosion. Third, 'last look' practices - during low liquidity, some providers can basically say 'Nah, changed my mind' and reject your trade. And weekends? Markets are technically closed, but some brokers keep prices moving with minimal liquidity - it's like trading in a ghost town.

§5Three scenarios that'll make it click

Let's compare some real situations:

| Scenario | Pair | Conditions | Spread | What Happens |

|---|---|---|---|---|

| Highway Driving | EUR/USD | London-NY overlap | 0.1-1 pip | Smooth sailing, instant execution, minimal cost |

| Country Road | AUD/CAD | Normal hours | 2-10 pips | Some bumps, decent execution, moderate cost |

| Off-Roading | Exotic pair | Asian session or news | 10-50+ pips | Bumpy ride, slippage likely, high transaction cost |

Imagine you're trading GBP/USD during major news. Spreads widen from 2 pips to 15 pips instantly. Your stop loss that should have cost you $20 now costs $150 just in spread. Ouch. Or picture trying to exit a large position in a minor pair when liquidity dries up - you might have to 'walk the book,' hitting worse and worse prices as you go. That's liquidity (or lack thereof) in action.

§6Where this 'liquidity' thing even came from

The word itself comes from Latin 'liquidus' - meaning fluid or flowing. Pretty fitting, right? The financial sense emerged in the early 20th century as markets got more organized. But the real lessons came from crises. During the 2008 financial meltdown, liquidity evaporated faster than ice cream in the sun. Banks stopped lending to each other, markets froze, and central banks had to flood the system with cash just to keep things moving. More recently, regulators like ESMA and FCA looked at all the retail traders blowing up accounts and said 'Hey, maybe 500:1 leverage isn't such a great idea.' So in 2018-2020, they capped leverage for retail traders - 30:1 for majors in the EU. COVID-19 in early 2020 gave us another masterclass in liquidity shocks - wild spreads, crazy volatility, and the reminder that when panic hits, liquidity is the first thing to run for the hills.

§7Key takeaways

- Liquidity is market 'thickness' - majors like EUR/USD have spreads as low as 0.1 pips, while exotics can hit 50+ pips during news.

- Low liquidity means wider spreads, slippage, and price gaps - three ways your trades can get expensive fast.

- Trade during peak hours (London-NY overlap) for best liquidity, avoid exotics and news events unless you know what you're doing.

- Respect leverage caps - 30:1 for majors in regulated jurisdictions exists for a reason. Thin liquidity + high leverage = trouble.

§8Frequently asked questions

QWhat's considered 'good' liquidity in forex?

QHow can I tell if a currency pair is liquid?

QWhy does liquidity change throughout the day?

QHow does low liquidity mess up my trades?

QIs high volatility the same as high liquidity?

§See also

§References

- Global Forex Market Statistics — Bank for International Settlements

- ESMA Product Intervention Measures — European Securities and Markets Authority