Here's a statistic that should make you pause: if you're using your bank's forex services for active trading, you're likely paying 5-20% in total fees before you even make a profit.

David van der Merwe

Trader de Mercados Emergentes ·  South Africa

South Africa

☕ 12 min de lectura

Lo que aprenderás:

- 1FNB Forex Contact: Official Channels and What They're For

- 2The SARB Rulebook: What You Can and Cannot Do

- 3The Silent Account Killer: FNB's Fees and Spreads

- 4FNB vs. A Retail Forex Broker: A Side-by-Side Comparison

- 5When You Should Actually Use FNB Forex Contact

- 6How South African Traders Get It Wrong (And How to Get It Right)

- 7Your Action Plan: From SARB to Screen

- 8The Bottom Line: It's a Service, Not a Strategy

Here's a statistic that should make you pause: if you're using your bank's forex services for active trading, you're likely paying 5-20% in total fees before you even make a profit. That's not a typo. While FNB provides a regulated service for travel money and international transfers, their model is fundamentally incompatible with the razor-thin margins of successful trading. I've seen more accounts blown up by misunderstood costs than by bad market calls. Let's break down exactly what FNB offers, who it's for, and why you should almost never use it as a trading platform.

First, let's get the practical details out of the way. FNB has separate teams for individuals and businesses, and their operating hours reflect a traditional banking model, not a 24/5 forex market.

For Individuals (Personal Forex):

- Phone: 0860 1 FOREX (36739)

- Email: forex@fnb.co.za

- Hours: Weekdays 08:00 - 17:00, Saturdays 08:00 - 12:00.

For Businesses (Commercial Forex):

- Phone: 087 0 EFOREX (336739)

- Email: fxsupport@rmb.co.za

International Callers:

- Individuals: +27 11 352 5902

- Non-resident queries: +27 11 352 5025

These channels are designed for specific, regulated transactions: getting travel cash, setting up international payments for studies or property, or managing business invoices. The advisors are there to help you navigate SARB's complex rules, not to discuss your EUR/USD scalping strategy. If you call them asking about use or chart patterns, you'll get a polite but confused response. I made this mistake early in my career, thinking a bank's 'forex desk' was the same as a broker's trading desk. It's not.

Warning: FNB's forex service is a facilitation desk for regulated capital movement. It is not a trading platform. Expect no market analysis, real-time quotes for trading, or use beyond 1:1.

This is where most South African traders get tripped up. You're not just trading against the market; you're trading within one of the world's stricter regulatory frameworks. The South African Reserve Bank (SARB) and the Financial Sector Conduct Authority (FSCA) control everything.

The Core Rule: It is illegal to buy or sell foreign currency outside authorised channels. Full stop. That means no backroom deals, no 'friend of a friend' offering you USD. You must use a bank like FNB or a licensed dealer.

Your Personal Allowances (The Big One): As a resident, you have two annual allowances:

- Single Discretionary Allowance (SDA): R2 million. No tax clearance needed. Use it for travel, gifts, online shopping.

- Foreign Investment Allowance (FIA): R10 million. Requires a Tax Clearance Certificate from SARS. This is for investing offshore - buying stocks, property, or funding an international brokerage account.

The Critical Detail for Traders: If you want to fund an international retail broker (like IC Markets or Pepperstone), you must use your FIA and get that tax clearance. You cannot use your SDA for this purpose. I learned this the hard way in 2015 when a R150,000 transfer to a broker was rejected and my bank account was flagged for a compliance review. It took three weeks to sort out.

Travel-Specific Rules:

- You can't buy travel forex more than 60 days before your trip.

- You must show a valid ticket and passport.

- Unused cash must be sold back within 30 days of returning.

- You can only physically carry R25,000 in SARB banknotes out of the country.

Crypto Grey Area: You can use your allowances to send money abroad to buy crypto on an international exchange. However, you cannot then send that crypto asset back out of South Africa. It's a one-way street for now.

“Using FNB for active trading is like using a cargo ship to compete in a speedboat race.”

This is the heart of the matter. Banks are not built for cost-efficient trading. Their profit model is based on large spreads and layered fees. Let's look at the numbers, which are brutal for any active trader.

Transfer Fees (Sending Money Abroad)

- Under R10,000: Fixed fee of R100 - R200.

- Over R10,000: 0.55% commission (min R275, max R550).

The Hidden Monster: The Exchange Rate Margin

This is where they really get you. FNB doesn't give you the interbank rate. They add a margin on top. For major currencies like USD, EUR, and GBP, this margin is typically 1% to 4%. For exotic or emerging market currencies, it can shoot up to 4.5% or more.

Let's do the math with a real example from last year. A client wanted to send £10,000 to the UK for a property deposit.

- Interbank rate that day: 1 GBP = R23.00

- FNB's offered rate (with a 2.5% margin): ~1 GBP = R23.575

- Cost of the margin: R0.575 per pound.

- Total hidden cost on £10,000: R5,750.

On top of that, add the 0.55% commission (R275 on R230,000). Your total cost to move the money is over R6,000 before it even lands. For a trader, this is suicide. If you're swing trading and aim for a 5% return on a position, you've just given up half your potential profit to bank fees alone.

Example: You use R100,000 of your allowance to fund a trading account.

- FNB Exchange Rate Margin (avg. 3%): -R3,000

- Transfer Commission (0.55%): -R550 Money that actually reaches your broker: R96,450 You are immediately down 3.55%. To just break even on the transfer, your first trade needs to make 3.7%. Most professional traders struggle to consistently achieve that per trade.

Receiving money has similar fees (0.55% commission, plus another margin when converting back to ZAR). The round-trip cost can easily wipe out 5-10% of your capital. Compare this to a retail broker where the spread on EUR/USD might be 0.1 pips (a fraction of a percent), and the difference is staggering.

💡 Consejo de Winston

The bank's spread isn't a fee, it's a trench you have to climb out of before you even start fighting. A 3% margin means you need a 3.1% gain just to break even on the transfer. How many of your trades hit that?

This isn't about which is 'better' in a general sense. It's about using the right tool for the job. Using FNB for active trading is like using a cargo ship to compete in a speedboat race.

| Feature | FNB (Bank Forex) | Retail Broker (e.g., Exness, XM) |

|---|---|---|

| Primary Purpose | Regulated capital transfer, travel money. | Speculative trading on price movements. |

| use | Effectively 1:1 (you send your own capital). | Up to 1:500 (FSCA regulated) or higher offshore. |

| Cost Structure | Large %-based spreads (1-4.5%) + fixed commissions. | Tight spreads (often <0.1% on majors) + possible commission. |

| Trading Platform | None. You make a phone/online transfer order. | MT4/MT5, cTrader with charts, indicators, automated trading. |

| Market Access | Spot FX for delivery. | Spot FX, CFDs on indices, commodities, crypto. |

| Speed of Execution | Hours to days for a transfer to settle. | Milliseconds for trade execution. |

| Regulatory Focus | SARB Exchange Control (moving money). | FSCA Market Conduct (fair trading). |

The use Trap (and Salvation): Banks don't offer use for forex trading. You put up R100,000 to control R100,000. At a broker, with 1:100 use, you control R10,000,000 with that same R100,000 margin. This is a double-edged sword. It magnifies both gains and losses, which is why most inexperienced traders blow up. But used with strict risk management - like a proper position size calculator - it allows for sensible risk (e.g., risking 1% of your account) on trades that can actually generate a meaningful return relative to costs.

The broker model is built for frequency and small margins. The bank model is built for occasional, large-value transfers. They are fundamentally different worlds.

“The round-trip cost of moving money through a bank can easily wipe out 5-10% of your capital before you place a single trade.”

Given all this, when does it make sense to pick up the phone and call 0860 1 FOREX?

- You're Traveling: This is their sweet spot. Getting your USD, EUR, or GBP cash for a holiday. They'll guide you through the documents and limits.

- Making a Large, Legitimate Offshore Payment: You're buying a property in the UK, paying for your child's university fees in Australia, or investing in a foreign stock market via a formal, long-term investment account. You need the tax clearance and the structured, auditable paper trail that a bank provides.

- Your Business Needs to Pay/Invoice in Foreign Currency: If your company imports goods or pays overseas contractors, FNB's business desk can set up foreign currency accounts and handle the commercial documentation.

- You're Cautious and Want Zero use: If you have a strong view on the ZAR and simply want to convert a lump sum of savings to another currency and hold it in a bank account abroad, using your allowance through FNB is the compliant way.

If your goal is to actively trade currency pairs multiple times a week or day, looking for small percentage moves, then this is not the service for you. The costs will eat you alive. You need the tight spreads and use of a dedicated broker, paired with a strategy built for that environment, like a disciplined scalping strategy.

I've coached hundreds of traders here. The mistakes are painfully consistent.

Mistake 1: Funding the Wrong Account with the Wrong Allowance. Trying to send money to an international broker using your Single Discretionary Allowance (SDA). It will be blocked. Solution: Always use your Foreign Investment Allowance (FIA) for broker funding. Get your Tax Clearance Certificate from SARS first. It's a hassle, but it's the only legal way.

Mistake 2: Ignoring the Total Cost of Ownership. Seeing a 'R100 transfer fee' and thinking it's cheap. Solution: Always ask for the total all-in rate. "What is the final Rand amount I will pay for exactly 10,000 US Dollars?" Then work backwards to calculate the effective percentage fee. You'll be shocked.

Mistake 3: Trading Without a Plan for Repatriation. You make profits in USD in your offshore broker account. How do you get it back? You must declare it as foreign income, and it will count against your future allowances. Solution: Keep careful records of every transfer out and every transfer back. Work with a tax consultant who understands forex trading income.

Mistake 4: Using Bank 'Trading' Platforms. Some local banks offer CFD trading platforms. They often have wider spreads, higher commissions, and less sophisticated tools than dedicated international brokers. I once tried trading XAU/USD on a local platform; the spread was over 50 cents, while my main broker had a 10-cent spread. That's an immediate R40 per ounce disadvantage on every trade.

Pro Tip: Before you fund any account, do a dry run. Calculate the total cost of sending R10,000 and then converting it back immediately. That round-trip cost is your first hurdle. If it's more than 1-2%, it's likely unsuitable for active trading.

💡 Consejo de Winston

SARB doesn't care about your 50-pip stop loss. They care about the paper trail. Your trading log is your first line of defense in an audit. Date, amount, rate, purpose. Every. Single. Time.

“FNB's forex team are administrators and compliance officers, not trading coaches. Don't call them for chart advice.”

Here is a step-by-step guide to doing this legally and cost-effectively.

Step 1: Get Your Tax Clearance. Go to SARS eFiling and apply for a Tax Clearance Certificate for 'Foreign Investment'. Have your affairs in order. This can take a few weeks.

Step 2: Choose a Reputable, Regulated International Broker. Do your research. Look for brokers regulated by top-tier authorities (ASIC, FCA, CySEC) that accept South African clients. Read our detailed reviews on IC Markets and Pepperstone as a starting point. Ensure they offer MT4/MT5.

Step 3: Initiate the Transfer via Your Bank. Contact your bank's forex desk (use the FNB forex contact numbers above). Tell them you wish to use your Foreign Investment Allowance to fund an overseas trading account for investment purposes. Provide your broker's banking details and your tax clearance. They will guide you through their forms.

Step 4: Start Small and Manage Risk Ruthlessly. When the money lands, do not go all in. The market will always be there. Start with a micro account or tiny position sizes. Your first goal is not to make money, but to not lose the money you just paid so much to get offshore. Use a position size calculator religiously. Understand what a margin call is before it happens.

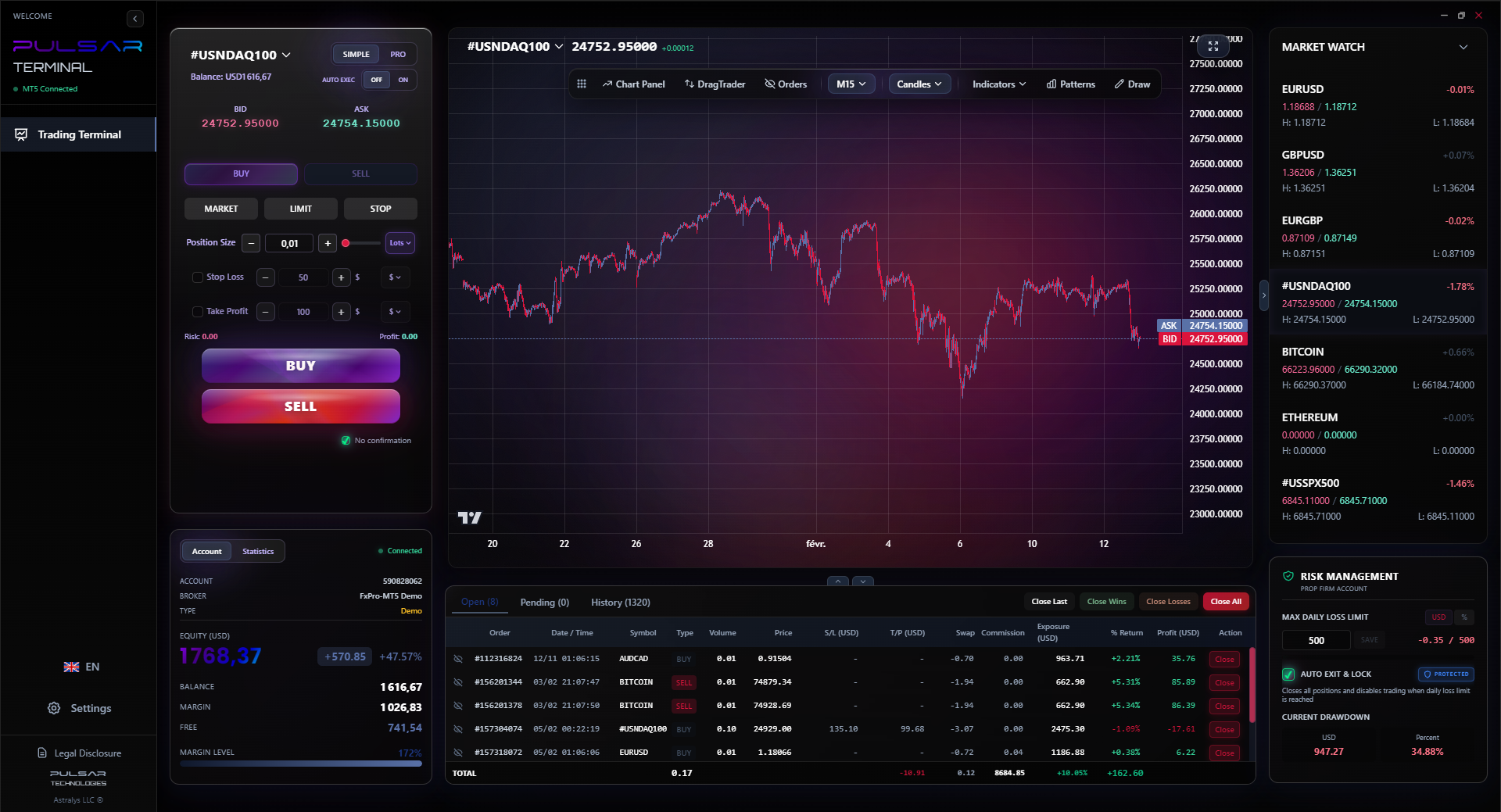

Step 5: Use Professional Tools. The default MT4/MT5 platform is limited. To manage complex trades, you need better order management. This is where tools like Pulsar Terminal come in, allowing for advanced stop-loss and take-profit strategies directly on your MT5 charts.

Step 6: Keep a Master Log. One spreadsheet: Date, Amount (ZAR), Exchange Rate Used, Fees, Amount Landed (USD). Do this for every single transfer in and out. It will save you endless pain with SARS later.

Managing complex trades with multiple take-profit levels and stop-losses is critical for risk management, and Pulsar Terminal's drag-and-drop order system on MT5 makes executing these strategies simple and precise.

Pulsar Terminal

La herramienta MT5 todo-en-uno: órdenes drag-and-drop, multi-TP/SL, trailing stop, grid trading, Volume Profile y protección prop firm. Usado por más de 1.000 traders diariamente.

FNB provides a vital, compliant service for South Africans needing to move money across borders. Their forex contact team are administrators and compliance officers, not trading coaches. For its intended purpose - facilitating travel, education, and investment under SARB's strict rules - it works.

However, for active currency trading, it's a prohibitively expensive channel. The combination of exchange rate margins and fixed fees creates a cost structure that is anathema to trading profitability. Successful trading hinges on managing tiny edges; starting 3-5% in the hole is a nearly insurmountable handicap.

Your journey should be: Use FNB to legally transfer a portion of your FIA to a low-cost, efficient international brokerage. Then, use that broker's infrastructure to trade. Keep FNB's number handy for when you need to bring profits home or for your next holiday. But don't confuse the two functions. One gets your capital to the battlefield; the other is where the battle is actually fought. Most traders fail because they never get this separation right, and they bleed out from a thousand small costs before they ever face the market's real challenge.

FAQ

Q1Can I use my FNB Forex allowance to trade with international brokers like IG or Plus500?

Yes, but you must use your Foreign Investment Allowance (FIA), not your travel allowance. This requires a Tax Clearance Certificate from SARS. You inform FNB you are transferring funds for the purpose of offshore investment. They will process the transfer to your broker's client money account.

Q2What is the difference between the R2 million and R10 million allowance?

The R2 million Single Discretionary Allowance (SDA) is for travel, gifts, and maintenance. No tax clearance needed. The R10 million Foreign Investment Allowance (FIA) is for investing offshore - stocks, property, or trading accounts. It requires a Tax Clearance Certificate. You can use both in a year, for a total of R11 million (R1m from the FIA overlaps).

Q3Why are FNB's forex rates so much worse than the rates I see on Google?

Google shows the mid-market (interbank) rate. FNB adds a margin (1-4.5%) to that rate to make their profit. This margin, not the small transfer fee, is the main cost. For a R100,000 transfer, a 3% margin costs you R3,000 instantly.

Q4Is it legal to use my offshore trading profits to buy crypto?

The rules are fluid. While you can use your ZAR allowances to send money abroad to buy crypto, using foreign currency earnings (like USD profits from trading) to buy crypto is a complex cross-border transaction. It's best to repatriate profits to South Africa first through proper channels and consult a specialist tax advisor, as SARB's view on this is still evolving.

Q5I'm back from holiday with leftover Euros. What should I do?

SARB rules state you must sell unused foreign banknotes back to an authorised dealer within 30 days of returning. Contact the FNB forex desk to sell them back. If you don't, and you're caught holding them beyond 30 days, you could face penalties and complicate future forex applications.

Q6Can FNB offer me use for trading like a forex broker?

No. FNB does not provide leveraged margin trading on currency pairs. They help the actual movement of your physical capital. For use, you must use a licensed retail forex broker or CFD provider, which is a completely different type of financial service.

Q7What documents do I need to buy forex for travel from FNB?

You will need a valid South African passport, a confirmed air ticket showing your departure date, and your FNB banking details. For larger amounts, they may ask for additional proof of the purpose of your travel.

Lección del Prof. Winston

Puntos clave:

- ✓Bank forex margins (1-4.5%) destroy trading profitability.

- ✓Use your R10m FIA, not your R2m travel allowance, for broker funding.

- ✓Always get a Tax Clearance Certificate from SARS first.

- ✓The real cost is the all-in rate, not the small transfer fee.

¿Te resultó útil este artículo?

Haz clic en una estrella

Análisis Trading Semanal

Análisis y estrategias semanales gratis. Sin spam.

Sobre el autor

David van der Merwe

Trader de Mercados Emergentes

Trader con sede en Johannesburgo con 11 años en divisas de mercados emergentes. Especialista en pares ZAR, trading regulado por la FSCA y análisis del mercado sudafricano.

Comentarios

Aviso de riesgo

El trading de instrumentos financieros conlleva un riesgo significativo y puede no ser adecuado para todos los inversores. El rendimiento pasado no garantiza resultados futuros. Este contenido tiene fines educativos únicamente y no debe considerarse asesoramiento de inversión. Siempre realice su propia investigación antes de operar.

También te puede interesar

Cara Trading Forex Sukses: 7 Prinsip dari Trader Profesional

Cara trading forex sukses dengan 7 prinsip trader pro: manajemen modal, disiplin, journal trading, backtest. Data nyata, bukan janji profit palsu.

Jam Trading Forex Terbaik untuk Trader Indonesia: Panduan Lengkap dengan Tabel Waktu

Panduan jam trading forex untuk trader Indonesia. Tabel 4 sesi dunia, jam emas 20:00-00:00, sesi mana yang harus dihindari. Data akurat + tips dari trader berpengalaman.

Top 5 Sàn Forex Uy Tín Nhất 2026: Review Jujur dari Trader Indonesia

Top 5 sàn forex uy tín 2026 untuk trader Indonesia. Review jujur: spread, deposit, withdraw, dukungan lokal. Exness, XM, IC Markets & lebih.

Obtener Pulsar Terminal

Todas estas calculadoras están integradas en Pulsar Terminal con datos en tiempo real de su cuenta MT5.

Obtener Pulsar Terminal