Instant funding prop firms are a trap for 95% of traders.

James Mitchell

वरिष्ठ ट्रेडिंग विश्लेषक

☕ 11 मिनट पढ़ने

आप क्या सीखेंगे:

- 1What Instant Funding Really Means (And What It Costs)

- 2How to Judge an Instant Funding Firm (Forget the Marketing)

- 3A Real Comparison of Top U.S.-Facing Instant Funding Firms

- 4The Looming Regulatory Shake-Up (This Changes Everything)

- 5The Psychological Trap: Why Instant Funding Sets You Up to Fail

- 6Who Actually Benefits from Instant Funding? (It's a Short List)

- 7How to Survive and Profit: A Risk Management Blueprint

- 8Final Verdict & What to Do Instead

Instant funding prop firms are a trap for 95% of traders. I know that sounds harsh, but after 12 years and watching hundreds of funded accounts get liquidated, the data doesn't lie. Giving a trader with poor risk management immediate capital is like handing a teenager the keys to a Ferrari. This article isn't just a list of the best instant funding prop firms; it's a breakdown of who they're actually for, the real costs you don't see, and the regulatory storm that's about to wipe half of them off the map. I'll show you the numbers that matter, not just the marketing hype.

Instant funding sounds simple: pay a fee, get a funded account, start trading. No challenge, no evaluation phase. The appeal is obvious, especially if you've failed a few traditional evaluations. But you're not buying capital; you're renting a simulated account with a promise of a profit split.

These firms operate as educational or technology service providers. Your 'funded' account is their proprietary capital in a simulated environment. When you profit, they pay you from their own pocket based on your simulated performance. This structure has kept them outside direct SEC or CFTC oversight as investment managers, but that's changing fast, which we'll get to.

The real cost isn't just the enrollment fee. It's the opportunity cost of not fixing the flaws that would have failed you in a challenge. I paid $299 once for a $25k instant account. I was up 8% in two days, got cocky, violated my own position size calculator rules on a EUR/USD trade, and gave it all back plus the daily loss limit in one session. The fee was gone, and I'd learned nothing new about my discipline.

Warning: The higher upfront fee for instant funding is often justified by skipping the 'hard part.' But the hard part - proving consistent, rule-based profitability - is the entire job. Skipping it doesn't make you a profitable trader; it just makes you an expensive demo trader.

💡 विंस्टन की सलाह

The fee for an instant account is the market's price for your lack of patience. The market always charges more for impatience than for skill.

Don't look at the shiny maximum account size. Look at the fine print that governs how you'll actually trade and get paid.

Profit Split & Payout Reality

A 90% profit split is meaningless if the payout threshold is impossible or they take 30 days to pay. You want clarity and speed. For example, a firm offering 80% with next-day payouts is often better than one offering 90% with bi-weekly payouts that get 'reviewed.' Your trading capital is your livelihood; cash flow matters.

Trading Rules That Make Sense

Scrutinize the daily loss, overall drawdown, and consistency rules. Some firms have a 'soft' daily loss that only triggers a warning, and a 'hard' overall drawdown that closes the account. Others have a single, strict daily loss limit. Know which you're dealing with. Also, check if they allow news trading, hedging, and overnight/weekend positions. If your scalping strategy relies on holding over a weekend, you need to know.

Platform & Instrument Access

Most use MetaTrader 4 or 5. But can you trade the instruments you're good at? If you're a gold trader, confirm they offer XAU/USD with reasonable spreads. Check if they allow EAs (Expert Advisors) if you use automated strategies.

Example: Let's say Firm A offers a $50k account with an 85% split, a 5% max loss rule, and weekly payouts. Firm B offers a $100k account with a 70% split, a 3% max loss rule, and daily payouts. For a trader making 3% per month, Firm A yields $1,275 monthly. Firm B yields $2,100 monthly, but the tighter 3% loss rule is 40% more restrictive. Which is 'better' depends entirely on your risk tolerance and strategy.

“You're not buying capital; you're renting a simulated account with a promise of a profit split.”

Here’s a breakdown based on current offerings, fees, and community reputation. Remember, this landscape is volatile, especially with new regulations.

| Firm | Example Instant Account Fee & Size | Profit Split | Key Rule (Example) | Payout Speed | Good For... |

|---|---|---|---|---|---|

| FundedNext | ~$500 for $50k | 80% - 90% | 5% Max Loss, No Daily Loss | 1-4 Biz Days | Traders who want no daily loss limit. |

| FTMO Instant | ~$400 for $50k | 80% (Up to 90%) | 5% Daily Loss, 10% Max Loss | 1-2 Biz Days | Traders familiar with FTMO's strict but clear rule set. |

| Blue Guardian | $65 for $5k (Standard) | 80% (Up to 90%) | 4% Daily Loss, 6% Max Loss | On-Demand (24-hr guarantee) | Traders who prioritize fast, reliable payouts above all. |

| FXIFY | From $69 | Up to 90% | Flexible Plans (2%-5% Daily Loss) | Weekly | Traders who want plan flexibility and use brokers like IC Markets. |

| City Traders Imperium | $299 for $5k | 80% - 85% | 3% Daily Loss, 5% Max Loss | Bi-Weekly | Disciplined traders comfortable with smaller, frequent payouts. |

My personal experience? I used FTMO Instant in 2023. The platform was solid, and a payout for $1,200 hit my account in exactly 36 hours. But their 5% daily loss rule is a tripwire. I saw a 4.8% drawdown on a volatile GBP move, which left me psychologically paralyzed for the rest of the day, afraid to hit that hard limit. The pressure felt different than with my own capital.

Pro Tip: Always calculate the 'break-even' point. If you pay a $400 fee for an account, you need to generate $400 in net profit just to get back to zero. With an 80% split, that means you must gross $500 in simulated profits before you see a dime of real money. That's your first real target.

💡 विंस्टन की सलाह

A firm's maximum account size is an advertisement. Its profit split payout speed is its report card. Always read the report card.

This is the part most prop firm reviews ignore, and it's the most important. The free-wheeling days are ending.

In February 2024, the SEC adopted new rules (3a5-4 and 3a44-2) that broadly redefine 'dealers.' The intent is to force more proprietary trading firms to register as dealers, which brings them under SEC and FINRA oversight, net capital requirements, and regular examinations. The compliance clock is ticking, with a deadline about 12 months from the effective date.

What does this mean for you? By late 2025 into 2026, expect a brutal consolidation. We've already seen 80-100 firms vanish between 2023-2024. The firms that survive will be the ones with real capital, strong legal structures, and transparent operations. The shady ones offering '100% profit splits no rules' will be gone.

Your risk shifts from just market risk to counterparty risk. Is the firm you're paying a fee to today going to be solvent and compliant tomorrow? When you request a $10k payout, will they have the cash and regulatory clearance to send it? This makes choosing a firm with a long track record and clear compliance intentions critical. It's why I'm wary of brand-new, hyper-aggressive firms, even if their terms look great.

This regulatory shift might also standardize rules and profit splits, reducing the 'wild west' competition but increasing safety for traders. It's a necessary, if painful, evolution.

“The psychological weight of 'real' funded capital hits immediately, leading to over-trading or paralysis.”

Here's the raw truth from a risk manager's desk. Instant funding bypasses the single most valuable part of a traditional challenge: the conditioning phase.

A one or two-phase evaluation forces you to trade under strict rules for a month or two. It's frustrating, but it builds discipline. It teaches you to manage a string of losses without blowing your drawdown. When you finally get funded, you've been conditioned to respect the rules.

Instant funding throws you into the deep end with no practice. The psychological weight of 'real' funded capital (even if simulated) hits immediately. This leads to two common blow-up patterns:

- Over-trading to 'make the fee back fast': You feel the need to justify the upfront cost immediately. This leads to taking sub-par setups, increasing position size beyond your plan, and inevitable ruin.

- Paralysis after a loss: That first 2-3% drawdown feels catastrophic because you're already thinking about the daily loss limit. You freeze, miss good setups, or worse, revenge trade to recover.

I've done both. On a $10k instant account, I once lost 2.5% on a single trade. Instead of stopping, I doubled my next position on a EUR/USD bounce play I hadn't even analyzed. I was down 4.9% in 20 minutes, one bad tick from a margin call. I sweated for an hour until I could close at a 4.5% loss. I was finished for the day, my confidence shattered. The account died a week later.

Instant funding removes the guardrails of the evaluation process, assuming you already have the discipline of a funded trader. If you did, you probably wouldn't need instant funding in the first place.

Instant funding isn't useless. It's just a specialized tool for a specific type of trader. You might be a candidate if:

- You're a Proven, Consistent Trader with a Verified Track Record: You have years of statements from a personal account or a previously funded account that lapsed. You need capital now, not in 2 months. The instant account is a conduit for your existing skill, not a test.

- You're Testing a New Strategy in 'Live' Conditions: You have a strong swing trading system but want to see its psychological and execution effects in a funded environment without a 30-day evaluation delay.

- You're Transitioning from a Different Firm: Your previous prop firm changed rules or shut down, and you need a new home quickly to maintain income flow.

If you're a beginner, coming off a string of failed challenges, or still emotionally reactive to losses, you are not on this list. You are the target customer, and the statistical likelihood is that you will pay for an expensive lesson. Go back, pass a standard challenge from a reputable firm like FTMO or The5ers, and build the discipline first. The capital will still be there when you're ready.

💡 विंस्टन की सलाह

If you cannot be profitable with a 2% risk rule on a $10k demo, you will be destroyed with a 5% risk rule on a $100k 'instant' account. Scale the trader, not the account.

“The slow, boring way is almost always the fastest way to real, sustainable funding.”

If you decide to proceed, you must impose your own structure. The firm won't save you.

1. Treat the Fee as a Sunk Cost. The moment you pay it, that money is gone. Do not trade to recover it. Trade your plan, period.

2. Halve Your Normal Risk. If your strategy risks 1% per trade in your personal account, risk 0.5% on the instant funded account. The psychological pressure is higher, so reduce the mechanical pressure. This gives you more room for error and emotional breathing space.

3. Set Hard, Personal Daily Loss Limits. Even if the firm's daily loss is 5%, set your own at 2%. If you hit 2%, walk away. Your goal isn't to use all the risk capital they provide; it's to extract profit consistently.

4. Use Technology to Enforce Discipline. This is non-negotiable. You cannot rely on willpower. Use trade management tools that automate your exits. For example, a tool that can set a trailing stop or automatically move your stop to breakeven after a certain profit level removes emotional decision-making in the heat of the moment.

5. Document Everything. Keep a journal. Note your mental state before every trade. After a loss, write down what happened without blaming the market. This turns failures into data points, not disasters.

Following this blueprint won't guarantee success, but it will align your actions with the only thing that creates long-term profitability: consistent, rule-based process over unpredictable outcome.

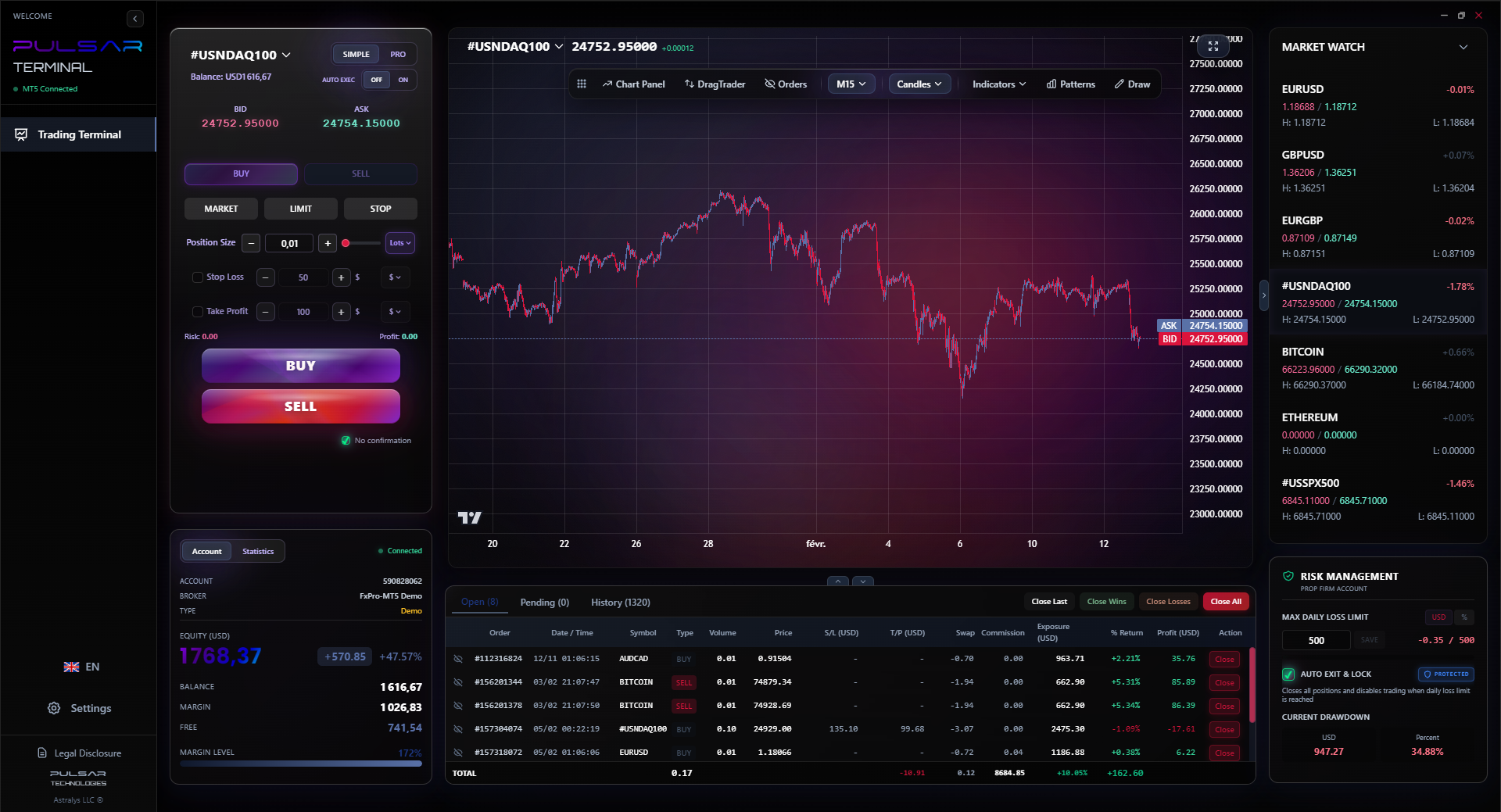

Imposing your own strict risk rules is critical, and Pulsar Terminal lets you automate those rules—like partial closures and trailing stops—directly on your MT5 platform, removing emotion from the equation.

So, what are the best instant funding prop firms? In the current climate, the 'best' are the ones most likely to survive the regulatory purge and pay you reliably: FundedNext, FTMO Instant, and Blue Guardian are strong contenders based on their established operations and clear terms.

But my broader verdict is this: for 80% of traders reading this, instant funding is a distraction from the real work. You're searching for a shortcut to capital, when you should be searching for a path to consistency.

Instead of spending $300 on an instant account, consider this alternative path:

- Fund a Small Personal Account: Deposit $500 with a reputable broker like Pepperstone or Exness. Your goal is not to get rich. Your goal is to produce three consecutive months of profitability, however small, while following a strict risk management plan (e.g., never risk more than 1% per trade).

- Then, Pass a Standard Challenge: Use the discipline you built to pass a traditional evaluation from a top-tier firm. The challenge fee will feel different because you've already proven you can manage real risk.

- Get Funded & Scale: Use the funded account to execute the same proven process. Scale your position size gradually as your confidence grows.

This path takes longer. It's less sexy. But it builds the foundation that instant funding assumes you already have. In trading, the slow, boring way is almost always the fastest way to real, sustainable funding.

FAQ

Q1Are instant funding prop firms legit?

The established ones with a multi-year track record and transparent payout histories are legitimate in the sense that they operate their stated business model. However, they are not banks or regulated investment managers. Your 'funded' account is typically a simulated account, and they pay you from their own capital based on your simulated performance. Their legitimacy hinges entirely on their ability and willingness to pay profits.

Q2What is the main disadvantage of instant funding?

The total lack of a conditioning phase. It places immediate live capital pressure on a trader who may not have proven they can trade under strict rules consistently. This leads to emotional decision-making and a very high failure rate, making the upfront fee a likely total loss for most.

Q3Can you make a living with instant funding prop firms?

A small minority of highly disciplined, already-profitable traders can and do. For them, it's an efficient capital access tool. For the vast majority, no. The volatility of trading, combined with the pressure of firm-specific rules, makes consistent income extremely difficult. It should not be considered a primary income source until you have a year or more of consistent, verified withdrawals.

Q4How fast are payouts from instant funding firms?

It varies widely. Some promise same-day or next-day (e.g., Blue Guardian), others process weekly or bi-weekly. Always check the firm's specific payout schedule and read user reviews about their adherence to it. A fast profit split is meaningless if the payout takes a month.

Q5Will new SEC regulations shut down instant funding firms?

Not necessarily shut down, but force massive consolidation. The new SEC rules will require many firms to register, meet capital requirements, and submit to oversight. Firms that can't or won't comply will close. By late 2025/2026, expect far fewer, but more stable and transparent, firms to remain.

Q6Should I choose instant funding or a challenge?

If you are new to prop firms or have failed challenges due to discipline/rule violations, choose a challenge. The evaluation phase is a valuable (and cheaper) training ground. Only choose instant funding if you have a verifiable history of disciplined, rule-based trading and need to bypass the time delay of an evaluation.

प्रो. विंस्टन का पाठ

:

- ✓The instant funding fee is a high-probability loss for undisciplined traders.

- ✓Prioritize payout speed and reliability over maximum profit split percentages.

- ✓Impose a personal daily loss limit 50% stricter than the firm's rule.

- ✓Regulatory changes in 2025 will separate legitimate firms from scams.

यह लेख कितना उपयोगी था?

रेट करने के लिए स्टार पर क्लिक करें

साप्ताहिक ट्रेडिंग विश्लेषण

मुफ़्त साप्ताहिक विश्लेषण और रणनीतियाँ। कोई स्पैम नहीं।

लेखक के बारे में

James Mitchell

वरिष्ठ ट्रेडिंग विश्लेषक

न्यूयॉर्क में स्थित, 9 साल से अधिक का ट्रेडिंग अनुभव। प्रमुख USD पेयर्स, प्रॉप फर्म चैलेंजेज और अमेरिकी नियामक परिदृश्य पर फोकस।

टिप्पणियाँ

आपको यह भी पसंद आ सकता है

Cara Trading Forex Sukses: 7 Prinsip dari Trader Profesional

Cara trading forex sukses dengan 7 prinsip trader pro: manajemen modal, disiplin, journal trading, backtest. Data nyata, bukan janji profit palsu.

Jam Trading Forex Terbaik untuk Trader Indonesia: Panduan Lengkap dengan Tabel Waktu

Panduan jam trading forex untuk trader Indonesia. Tabel 4 sesi dunia, jam emas 20:00-00:00, sesi mana yang harus dihindari. Data akurat + tips dari trader berpengalaman.

Top 5 Sàn Forex Uy Tín Nhất 2026: Review Jujur dari Trader Indonesia

Top 5 sàn forex uy tín 2026 untuk trader Indonesia. Review jujur: spread, deposit, withdraw, dukungan lokal. Exness, XM, IC Markets & lebih.

All these calculators are built into Pulsar Terminal with real-time data from your MT5 account. One-click position sizing, automatic risk management, and instant calculations.