Drawdown

DRAW-downsince Before 1797 (mentioned by Mary Wollstonecraft)Drawdown — dip your account takes from its highest point — think of it as the market's way of testing your patience.

§1So, what IS this 'drawdown' everyone keeps talking about?

Okay, picture this: you're climbing a mountain. That peak you just reached? That's your account hitting its highest value. Now, you slip a bit on some loose rocks and slide down the slope before finding your footing again. That slide? That's your drawdown. It's simply how far your account dips from its highest point before climbing back up. It's not necessarily a permanent loss — you might still be higher than where you started your climb! But it measures the 'ouch' factor, the volatility of your journey. Think of it as your account's personal rollercoaster drop. I've seen traders blow accounts because they ignored this simple metric, treating every dip like it didn't matter. Trust me, it does.

§2The math (don't worry, it's friendlier than it looks)

I know, formulas can make you want to close the browser. But stick with me — this one's actually simple. We just want to know what percentage of your peak you lost on the way down. Here's the magic: Drawdown (%) = ((Peak Value – Trough Value) / Peak Value) × 100. Peak Value is your account's all-time high (so far). Trough Value is the low point it hits after that peak, before making a new high. You subtract the trough from the peak, divide by the peak, and multiply by 100 to get a percentage. That's it! No calculus, I promise. This little number tells you exactly how deep the valley was between two mountains.

§3Let's walk through it with a real trading story

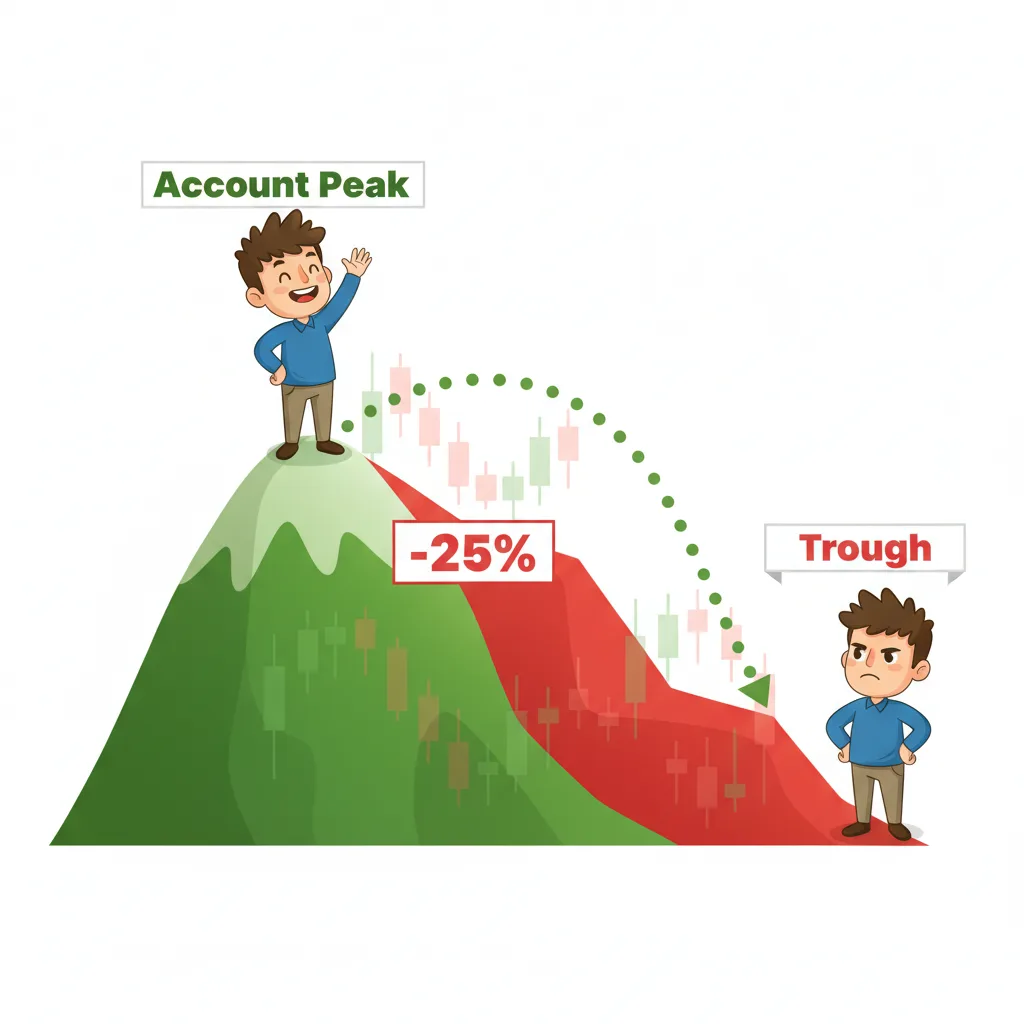

Imagine your account starts with $10,000. You trade well, and it grows to $12,000 — congrats, that's your peak! Then, a few trades go against you (it happens to the best of us), and your balance drops to $9,000 before things turn around. That $9,000 is your trough. So, your drawdown is: (($12,000 - $9,000) / $12,000) × 100. That's ($3,000 / $12,000) × 100, which equals 25%. See? Even though you're still up from your initial $10,000, you experienced a 25% drawdown from your peak. That's the number that keeps risk managers up at night.

§4The tricky bits and rulebook fine print

Now, here's where it gets spicy. First, JPY pairs like USD/JPY quote with two decimals (e.g., 155.25), not four like EUR/USD. This changes pip values, which affects how much a price move hits your wallet and thus your drawdown size. Second, if you trade with a prop firm or certain brokers, they often have strict daily drawdown limits. Exceed that in a single day, and poof — account gone. They might also set a maximum drawdown from your starting balance. These rules can be based on your equity (including open trades) or just your closed balance, with equity-based being the stricter hall monitor. Always read the fine print!

§5Three scenarios that'll make this crystal clear

Let's get concrete. Imagine you go long on EUR/USD at 1.0800 with $10k. Price rises to 1.0850, and your equity peaks at $10,500. Then it pulls back, and your equity dips to $10,200 before recovering. Drawdown = (($10,500 - $10,200) / $10,500) × 100 ≈ 2.86% — a gentle breeze. Now, a riskier scenario: your $10k account hits $15k, then crashes to $7,500. Drawdown = (($15,000 - $7,500) / $15,000) × 100 = 50%. That's a halving from the peak! Here's a quick comparison:

| Scenario | Peak Equity | Trough Equity | Drawdown | Feeling |

|---|---|---|---|---|

| Gentle Pullback | $10,500 | $10,200 | ~2.86% | "No biggie" |

| Major Crash | $15,000 | $7,500 | 50% | "Time for a walk" |

The bigger the drop, the harder the comeback — a 50% drawdown needs a 100% gain just to break even!

§6A quick history lesson (with less dust)

The term 'drawdown' has been around since at least the late 1700s — Mary Wollstonecraft used it before 1797! But in trading, it really came into focus as a key risk metric when people started seriously measuring performance. Events like the 2008 financial crisis screamed the importance of understanding downside risk. Suddenly, everyone cared about how far portfolios could fall. More recently, regulations like the FCA's leverage caps in 2020 indirectly affect drawdown by limiting how much you can amplify losses (and gains). So, while the word is old, its role as your trading dashboard warning light is very modern.

§7Key takeaways

- Drawdown is your account's dip from peak to trough — it's the market's way of testing your nerve.

- Aim to keep drawdown below 10% like the pros do; past 20%, you're playing with fire.

- A 50% drawdown needs a 100% gain just to break even — that's why small losses are easier to recover from.

- Always check broker rules for daily or maximum drawdown limits, or you might get an unexpected timeout.

§8Frequently asked questions

QWhat's a good drawdown percentage?

QHow do you calculate drawdown?

QIs drawdown the same as a loss?

QHow can I recover from a big drawdown?

QWhy is drawdown so important?

§See also

§References

- Historical usage of 'drawdown' — Etymology references

- FCA Leverage Cap Regulations — Financial Conduct Authority