Most traders I talk to think FNB Business Forex is just another trading platform.

David van der Merwe

เทรดเดอร์ตลาดเกิดใหม่ ·  South Africa

South Africa

☕ 10 นาทีอ่าน

สิ่งที่คุณจะได้เรียนรู้:

Most traders I talk to think FNB Business Forex is just another trading platform. They're wrong. I made that mistake myself years ago, trying to use it for day trading EUR/USD and getting absolutely hammered on spreads. The truth is, FNB's business forex services are built for a completely different purpose: managing real-world business currency flows, not speculative trading. This guide will walk you through exactly what it is, when to use it, and when to run straight to a proper FSCA-regulated broker instead.

Let's clear this up first. FNB Business Forex isn't a MetaTrader platform where you scalp the Yen. It's a suite of banking services designed for South African companies that deal with international money. Think import/export businesses, freelancers getting paid in USD, or companies paying overseas suppliers.

The core product is the FNB Business Global Account (CFC). This lets you hold money in 33 different currencies. So if you're an exporter getting paid in US Dollars, you can keep those dollars in a USD sub-account instead of converting to Rand immediately. This is huge for managing currency risk on actual business income.

Warning: This is NOT for trading. The spreads on conversion are for wholesale/banking, not competitive for trying to profit from currency moves. I learned this the hard way. Back in 2019, I tried to use a similar business account from another bank to "trade" by timing conversions. The 1.5% margin they took on a USD/ZAR conversion wiped out any potential gain from my "clever" timing. It was a rookie move.

Where FNB does touch trading is through their FNB Share Investor platform. It's more of a traditional CFD/Forex offering, but honestly, it's not where serious traders hang out. The tools are basic, and the costs aren't as sharp as dedicated brokers like Pepperstone or Exness. For a business needing to hedge a real invoice, it's a bank service. For a trader wanting to profit, it's a broker's world.

“FNB Business Forex is built for managing real-world business currency flows, not speculative trading.”

FNB's pricing is a mix of commissions and exchange rate margins. You need to understand both, or you'll get a nasty surprise.

The Commission Structure

For international payments sent or received online over R10,000, it's a 0.55% commission. There's a minimum and maximum, though. Sending has a min of R275 and max of R550. Receiving has a min of R175 and max of R450. For smaller amounts, fixed fees kick in.

The Hidden Bite: The Exchange Rate Margin

This is the real cost. FNB adds a margin to the interbank exchange rate. For major currencies like USD, GBP, or EUR, this is typically between 1% and 4%. Let's do the math everyone misses.

Example: You need to pay a supplier $10,000. The interbank rate is 18.50 ZAR/USD. With a 2% margin, your rate becomes roughly 18.87. That extra 37 cents per dollar means you're paying R3,700 more for that $10,000 payment. That's R3,700 gone before your goods even ship.

There's also a potential R130 fee if a payment is sent or received in ZAR. Always check the latest pricing guide on their website, as these details do shift.

The "Free" Account That Isn't Free

They advertise the Business Global Account with no monthly fees and no minimum balance. That's true. But the cost is in the margin when you convert or move money. It's a classic banking model: the product is free, but the transactions fund it. For holding currency without immediate conversion, it's genuinely useful. For active moving, the costs add up fast.

💡 เคล็ดลับจาก Winston

A bank's forex service is for moving money. A broker's platform is for making money from movement. Confuse the two, and the only thing moving will be your capital out of your account.

“The main 'hidden' cost isn't the commission; it's the 1-4% exchange rate margin baked into your conversion.”

This is the part that gives every South African business owner a headache, but you must get it right. The South African Reserve Bank (SARB) controls this space with an iron fist via Exchange Control Regulations.

The 180-Day Rule is the big one. If your business earns foreign currency, you generally have to bring it back to South Africa and convert it to Rand within 180 days from when it was due. You can't just leave it sitting in an offshore account indefinitely without SARB approval. I've seen clients get tripped up by this, thinking their USD earnings in their FNB Global Account were "offshore." They're not. It's still within the South African banking system and subject to the rule.

Balance of Payments (BoP) Reporting is another. Every time you make an international payment through FNB, you have to give a reason code. Buying software? Paying for imports? Investing? There's a code for that. FNB reports this to SARB. It's not optional.

Allowances for Individuals/Businesses: If you're moving money for investment, know the limits. The Single Discretionary Allowance (SDA) lets you move up to R1 million a year abroad without tax clearance. The Foreign Investment Allowance (FIA) allows up to R10 million, but you need a Tax Compliance Status PIN from SARS. This is more for personal wealth, but as a business owner, it blurs the lines.

For actual speculative trading, a different regulator steps in: the Financial Sector Conduct Authority (FSCA). Any platform you use for trading forex CFDs must be FSCA-regulated. FNB's Share Investor platform falls under this, but their Business Global Account services are under SARB's exchange control. Different worlds, different rules.

“The main 'hidden' cost isn't the commission; it's the 1-4% exchange rate margin baked into your conversion.”

This decision cost me money early on. Now, my rule is simple.

Use FNB Business Forex For:

- Hedging Real Business Flows: You have a known USD invoice to pay in 90 days. You can buy USD now and hold it in your Global Account, locking in the rate.

- Receiving Foreign Income: You're a consultant paid in Euros. Receive and hold Euros to avoid constant conversion fees.

- Making International Supplier Payments: Sending GBP to a UK manufacturer for goods. The paper trail and BoP coding through your bank is clean and compliant.

- Security & Integration: Having everything in one FNB online banking view is convenient for business management.

Use a Regulated Forex Broker (like IC Markets or XM) For:

- Speculative Trading: Trying to profit from movements in EUR/USD or XAU/USD.

- Advanced Strategies: Scalping, swing trading, using complex indicators like the MACD or RSI.

- Better Pricing: Brokers offer raw spreads from 0.0 pips. A typical spread on EUR/USD at a good broker might be 0.1 pips. At a bank, the equivalent margin could be 100+ pips. It's a different universe.

- use & Advanced Tools: Brokers offer use (responsibly, of course) and platforms like MT4/MT5 with proper charting, automated trading, and tools like Pulsar Terminal for advanced order management.

Mixing the two will lead to poor results. I once tried to use a business currency account to "average down" a position over weeks like a trade. The fees made it pointless. Keep business banking for business, and trading for trading platforms.

💡 เคล็ดลับจาก Winston

That 1-4% margin FNB adds? On a R1 million conversion, that's R10,000 to R40,000 gone before you even start. In trading, we call that a terrible entry price. In business, you call it a cost of operation. Know which game you're playing.

“Using a business currency account to trade is like using a cargo ship to win a speedboat race.”

If you've decided you need the Business Global Account, here's what to expect. It's more involved than opening a trading account.

- Eligibility: You need an existing FNB business account. This is for registered businesses, not sole proprietors using personal accounts for side hustles.

- The FICA Haul: Get your documents ready. Certified ID copies of directors/members, business registration documents (CIPC), proof of address for the business. Standard stuff, but have it all prepared.

- Apply Online or In-Branch: For single-member entities (like a PTY with one director), you can open sub-accounts in 9 major currencies (USD, GBP, EUR, etc.) directly online via the FNB Business Online Banking. For more complex entities or other currencies, a branch visit might be needed.

- Understand the Limits: The account is subject to SARB's exchange controls. You'll need to declare the source of foreign funds and the purpose for any conversions or payments. This is normal compliance.

- Using It: Once open, you'll see your main ZAR account and the foreign currency sub-accounts. You can transfer between them (which triggers the exchange rate margin) or receive payments directly into, say, your USD account.

For the FNB Share Investor platform for trading, it's a separate application within their investment wing. It links to your banking profile, but the sign-up is specific to trading. Remember, the tools here are basic. If you're serious about chart analysis, you'll outgrow it quickly.

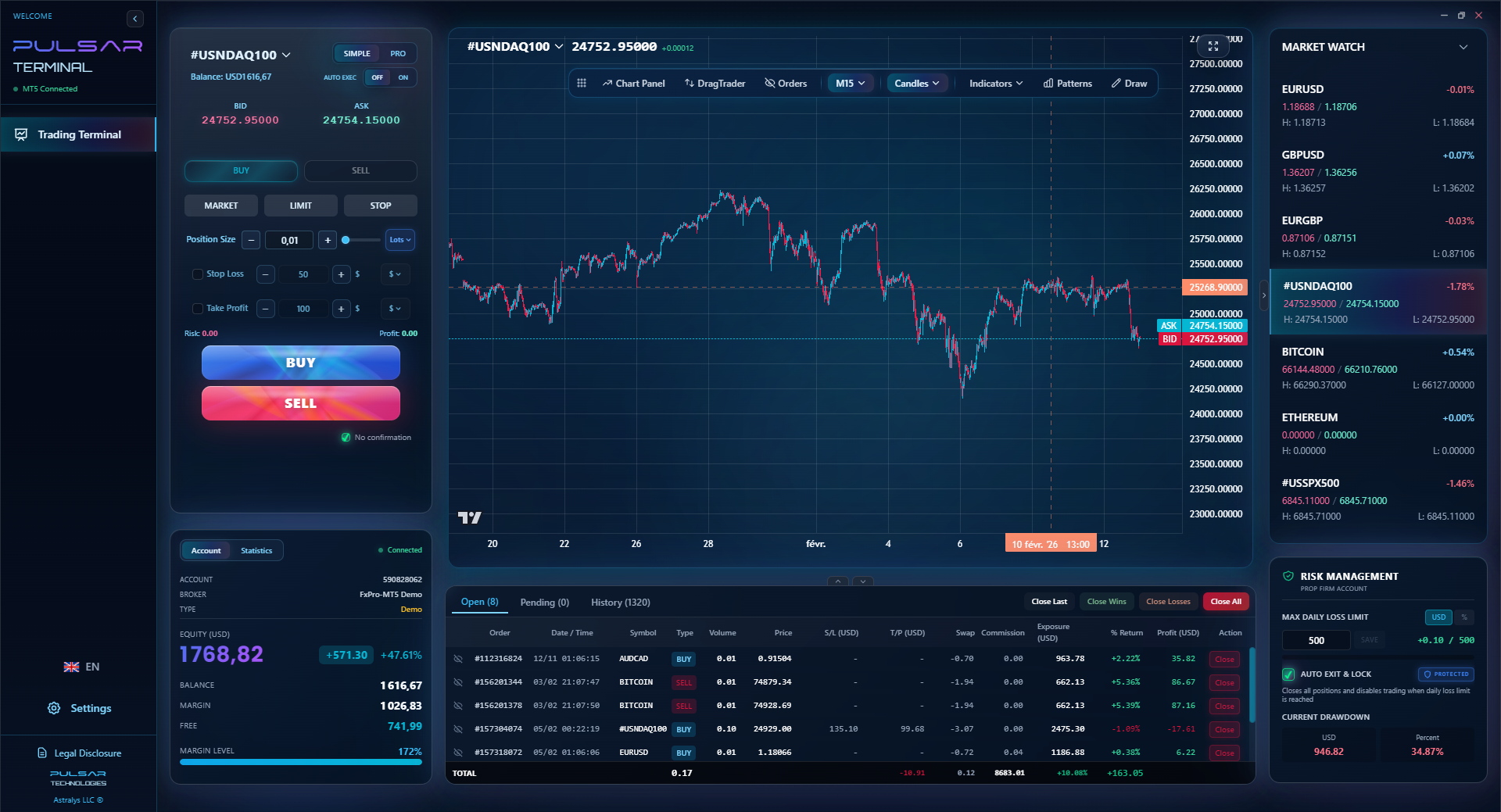

Managing complex trades requires precise tools, which is why serious traders use platforms like Pulsar Terminal on MT5 for advanced order types and risk management far beyond what basic banking platforms offer.

Pulsar Terminal

เครื่องมือ MT5 ครบวงจร: ลากวางคำสั่ง, multi-TP/SL, trailing stop, grid trading, Volume Profile และการป้องกัน prop firm ใช้งานโดยเทรดเดอร์กว่า 1,000 คนทุกวัน

“Using a business currency account to trade is like using a cargo ship to win a speedboat race.”

I've seen these mistakes repeated. Don't let it be you.

Pitfall 1: Using it as a Trading Account. This is the biggest one. The spreads/margins are for facilitating business payments, not competing with the interbank market. You will lose trying to day-trade here.

Pitfall 2: Ignoring the 180-Day Rule. You get a $50,000 payment and leave it in your USD Global Account for 8 months, thinking you're smart waiting for a better ZAR rate. SARB may flag this, and you could face penalties. Plan your currency conversions with this deadline in mind.

Pitfall 3: Misunderstanding the Costs. Focusing only on the 0.55% commission and forgetting the 1-4% exchange rate margin. The margin is the main cost. Always ask for the all-in rate – the final ZAR amount you'll pay or receive after all fees and margins.

Pitfall 4: Poor Timing on Large Conversions. You need to convert ZAR 2 million to USD for a supplier payment. Doing it in one go exposes you to the rate at that single moment. Some businesses use a forward contract (which FNB can arrange) to lock in a rate for a future date. Or, if allowed by cash flow, they might convert smaller chunks over time (averaging). This isn't trading; it's treasury management.

Pitfall 5: Not Shopping Around. For large, regular international payments, don't assume your bank is the cheapest. Specialist currency firms sometimes offer better rates for bulk transfers. It's worth getting a few quotes, especially for amounts over R500k.

💡 เคล็ดลับจาก Winston

SARB's 180-day rule isn't a suggestion. I've seen sharp traders turn into panicked business owners trying to explain why currency was sitting idle. Manage your business liquidity like you manage your trading stop-loss: with a clear plan and discipline.

“Keep business banking for business, and trading for trading platforms. Mixing the two will lead to poor results.”

The market isn't static. Here's what's shaping the next few years.

Regulatory Tightening is Real. The FSCA is pushing all brokers to get Over-the-Counter Derivatives Provider (ODP) licenses. This means more capital, better client protection, and stricter rules. It's a good thing for trader safety but means the cowboy days are over. SARB also constantly tweaks its guidelines.

Digital Everything. The move to online platforms is complete. FNB's app and online banking are where 99% of these transactions happen. For traders, platforms like MetaTrader 5 with advanced add-ons are becoming standard. The convenience of managing a business hedge from your phone is powerful.

Market Growth. The stats are solid. South Africa's forex market hit over USD 3.8 billion in 2024 and is growing steadily. That means more competition, better services, and more sophisticated tools becoming available locally.

The Bottom Line: FNB Business Forex is a strong, compliant tool for its specific job. It's not sexy, it's not for getting rich quick on pip movements, but it's essential infrastructure for a South African business operating globally. For the trading side of your brain, that's what your FSCA-regulated broker and a solid position size calculator are for. Keep them separate, use them for their intended purposes, and you'll manage both your business finances and your trading capital a whole lot better.

FAQ

Q1Can I use my FNB Business Global Account to trade forex for profit?

No, you really shouldn't. It's designed for holding and converting currency for genuine business needs. The exchange rate margins (1-4%) are far too wide for profitable trading. You'd be competing with professional traders who pay spreads as low as 0.1 pips on dedicated platforms. Use an FSCA-regulated broker for speculative trading.

Q2What is the 180-day rule and how does it affect my FNB account?

It's a SARB rule stating that most foreign currency earnings must be repatriated to South Africa and converted to ZAR within 180 days. If you receive USD into your FNB Business Global Account (a South African account), it's considered repatriated. You don't necessarily have to convert it immediately, but the clock starts ticking, and you need to be able to justify holding it for business purposes. Leaving it there indefinitely as a "trade" could lead to compliance issues.

Q3Are there any hidden fees with the FNB Business Global Account?

The account itself has no monthly fee. The costs are in the transactions. The main 'hidden' cost is the exchange rate margin (1-4% added to the market rate). You also pay a commission (0.55% for larger transfers) and potentially a R130 fee for Rand-based cross-border payments. Always ask for the final all-in rate before confirming a conversion.

Q4How does FNB Business Forex compare to using a broker like Pepperstone?

They serve different masters. FNB is for business banking: making payments, receiving income, and hedging real currency exposure. Pepperstone is for trading: speculating on price movements with tight spreads, use, and advanced charts. It's like comparing a cargo ship (FNB) to a speedboat (Pepperstone). Use the right tool for the job.

Q5What documents do I need to open a Business Global Account?

Standard business FICA: Certified IDs of all directors/members, your company's CIPC registration documents, and proof of business address (like a utility bill). If you're a non-resident entity, you'll need a foreign passport, permit, and proof of where the funds originated.

Q6Can I open sub-accounts in any currency?

FNB offers 33 currencies, but for single-member entities applying online, you can typically open in 9 major ones: USD, GBP, EUR, AUD, CAD, CHF, AED, CNY, and INR. For other currencies or more complex business structures, you may need to apply via your relationship manager or in a branch.

Q7Is my money safe in an FNB Business Forex account?

It's held as bank deposits with First National Bank, a major South African financial institution. It's covered by the same protections as your normal business account. This is different from funds held with a forex broker, which are held in segregated client money accounts under FSCA rules. Both are regulated, but under different frameworks for different purposes.

บทเรียนจาก Prof. Winston

สรุปสาระสำคัญ:

- ✓FNB's service is for payments & hedging, not trading.

- ✓The real cost is the 1-4% exchange rate margin.

- ✓SARB's 180-day rule is non-negotiable for businesses.

- ✓Always compare the all-in rate before converting.

- ✓Use FSCA brokers for trading, not bank platforms.

บทความนี้มีประโยชน์แค่ไหน?

คลิกดาวเพื่อให้คะแนน

ข้อมูลเชิงลึกการเทรดรายสัปดาห์

การวิเคราะห์และกลยุทธ์รายสัปดาห์ฟรี ไม่มีสแปม

เกี่ยวกับผู้เขียน

David van der Merwe

เทรดเดอร์ตลาดเกิดใหม่

เทรดเดอร์ประจำโจฮันเนสเบิร์ก มีประสบการณ์ 11 ปีในสกุลเงินตลาดเกิดใหม่ เชี่ยวชาญคู่ ZAR การเทรดภายใต้กฎระเบียบ FSCA และการวิเคราะห์ตลาดแอฟริกาใต้

ความคิดเห็น

คำเตือนความเสี่ยง

การซื้อขายตราสารทางการเงินมีความเสี่ยงสูงและอาจไม่เหมาะสำหรับนักลงทุนทุกคน ผลการดำเนินงานในอดีตไม่ได้รับประกันผลลัพธ์ในอนาคต เนื้อหานี้มีวัตถุประสงค์เพื่อการศึกษาเท่านั้นและไม่ควรถือเป็นคำแนะนำในการลงทุน โปรดทำการวิจัยของคุณเองก่อนการซื้อขาย

คุณอาจชอบสิ่งนี้

Cara Trading Forex Sukses: 7 Prinsip dari Trader Profesional

Cara trading forex sukses dengan 7 prinsip trader pro: manajemen modal, disiplin, journal trading, backtest. Data nyata, bukan janji profit palsu.

Jam Trading Forex Terbaik untuk Trader Indonesia: Panduan Lengkap dengan Tabel Waktu

Panduan jam trading forex untuk trader Indonesia. Tabel 4 sesi dunia, jam emas 20:00-00:00, sesi mana yang harus dihindari. Data akurat + tips dari trader berpengalaman.

Top 5 Sàn Forex Uy Tín Nhất 2026: Review Jujur dari Trader Indonesia

Top 5 sàn forex uy tín 2026 untuk trader Indonesia. Review jujur: spread, deposit, withdraw, dukungan lokal. Exness, XM, IC Markets & lebih.

รับ Pulsar Terminal

เครื่องคำนวณทั้งหมดนี้ถูกสร้างไว้ใน Pulsar Terminal พร้อมข้อมูลเรียลไทม์จากบัญชี MT5 ของคุณ

รับ Pulsar Terminal