Let's clear up the biggest misconception right now.

David van der Merwe

Gelişen Piyasalar Yatırımcısı ·  South Africa

South Africa

☕ 10 dk okuma

Neler öğreneceksiniz:

Let's clear up the biggest misconception right now. When most South Africans hear 'netbank forex,' they think of Nedbank's online platform for sending money overseas or buying travel cash. They assume that's 'forex trading.' It's not. Not even close. That confusion has cost new traders more money than any bad trade ever could. Using a bank for forex transactions and using a broker for forex trading are two completely different worlds with different rules, costs, and purposes. I'll walk you through both, show you the shocking numbers, and explain exactly where you should be putting your money if you actually want to trade.

In South Africa, 'netbank forex' typically refers to the foreign exchange services offered through your bank's online portal - Nedbank, ABSA, FNB, Standard Bank. This is for transactions: paying an overseas supplier, receiving funds from abroad, loading a travel card, or converting ZAR to USD for a holiday. It's a utility service, not an investment platform.

The critical distinction? You're a customer buying a product (foreign currency) from the bank. In forex trading with a broker, you're a speculator taking a position on price movements. The bank's goal is to provide you currency at a marked-up rate with fees on top. The broker's goal is to provide you a venue to speculate, making money on the spread or commission.

I learned this the hard way early on. I needed to send $5,000 overseas for a business expense via my bank. The exchange rate margin and fees ate nearly 3% of the total. I remember thinking, 'If I could just bet against this rate they're giving me, I'd make a fortune.' That was the lightbulb moment. The bank's service and the trading market are connected by the underlying price, but they are fundamentally different games. One is for moving money; the other is for making money from money moving.

Warning: Never, ever confuse your bank's forex transfer rate with the live trading rate on a platform like MT5. They are calculated differently, with the bank's rate always including a hefty built-in profit margin for them.

💡 Winston'ın İpucu

If your bank's forex rate looks 'good,' it's not. They're not a charity. That 'good' rate already has their 2-3% baked in. The real price is on the broker's platform.

“Using a bank for forex transactions and using a broker for forex trading are two completely different worlds.”

Let's talk numbers, because this is where the bank makes its money. These aren't hypotheticals; these are the published fees as of 2025/2026. We're not talking pips here, we're talking percentages that would make any trader's blood run cold.

Transfer Fees: The Obvious Bite

For a digital outgoing payment, Nedbank charges a 0.55% commission (min R198, max R750) plus a R140 'communication fee.' So, sending R100,000 overseas costs you at least R198 + R140 = R338 just in fees, before we even look at the exchange rate.

The Exchange Rate Margin: The Real Monster

This is the hidden cost. Banks don't give you the interbank rate. They add a margin. For major currencies (USD, EUR, GBP), Nedbank's margin is around 2.5%. For other currencies, it can soar over 5%. Let's do the math.

You want to convert R100,000 to USD. The real market rate (mid-price) is 18.50 ZAR/USD. That should get you $5,405.41. With a 2.5% margin, the bank gives you a rate of roughly 18.96 ZAR/USD. You now get $5,274.26.

📊 Example: You've just lost $131.15 (about R2,427) without seeing a single 'fee' line item. Combined with the transfer fees, your total cost on that R100k is pushing 3%. On a R1 million discretionary allowance, that's R30,000 gone before the money even leaves the country.

Travel Cards & Cash

It gets worse for physical cash. Buying foreign currency for travel carries a 2.15% commission (min R135). If you come back with leftover Euros and sell them back? Another 1.15% hit. This isn't trading; it's financial friction, pure and simple. For actual forex trading, your costs are measured in fractions of a percent - the spread definition on EUR/USD can be under 0.01% on a good broker account. The difference is astronomical.

“The bank's goal is to provide you currency at a marked-up rate. The broker's goal is to provide you a venue to speculate.”

This is the arena. You don't trade forex through Nedbank's app. You trade through a licensed broker that gives you access to the global interbank market via contracts for difference (CFDs) or other instruments.

The Regulator: Your First Safety Check

Every legitimate broker serving South African clients must be licensed by the Financial Sector Conduct Authority (FSCA). This isn't optional. The FSCA enforces rules like the 30:1 use cap for retail clients, segregates client funds, and provides a recourse path. Always, always check the FSP number. I only trust brokers with clear FSCA regulation or equivalent top-tier global licenses.

The Real Cost Structure: Pips & Commissions

Your costs as a trader are transparent. For major pairs like EUR/USD on a raw ECN account:

- Spread: As low as 0.0 pips.

- Commission: Typically $3-$7 per standard lot (100k units) per side.

So, opening and closing a 1-lot EUR/USD trade might cost you $10 total. On a $100,000 position, that's 0.01%. Compare that to the bank's 2.5%+. It's a different universe.

For ZAR pairs, which are exotic, spreads are wider but still competitive with brokers. USD/ZAR might have a 5-pip spread, and EUR/ZAR around 14 pips. Even that 14-pip spread on EUR/ZAR is about 0.07% at current rates - still orders of magnitude cheaper than a bank's margin. Brokers like IC Markets and Pepperstone are popular here for their tight spreads on these pairs.

Minimum Deposits & Capital

Forget the bank's millions. You can start trading with a broker for very little. XM allows a $5 minimum. Exness has no minimum on some accounts. But let's be real: starting with R500 is a recipe for a margin call. For serious practice, I'd say R1,500-R5,000. For meaningful trading with proper position size calculator use, think R20,000+. My first live account was R15,000, and even that felt tight managing more than one trade.

💡 Winston'ın İpucu

Your first R10,000 in trading isn't capital. It's tuition. Expect to pay it to the market to learn. The goal is to make the lessons cheap and the education permanent.

“On a R1 million discretionary allowance, that's R30,000 gone before the money even leaves the country.”

This is a crucial advantage local brokers offer. Many FSCA-regulated brokers offer ZAR-denominated trading accounts. This means you deposit and withdraw in Rands, and your profit/loss is calculated in ZAR. It eliminates the hidden forex conversion cost you'd get if you had a USD account with an offshore broker.

Payment Methods That Actually Work

South African banks are legally required to police exchange controls. Trying to send R200,000 to an unregulated offshore broker will get blocked. Using an FSCA-regulated broker simplifies this.

- Local EFT/Ozow: The easiest. Money moves from your bank to the broker's local South African bank account. Usually free, takes a few hours.

- Credit/Debit Cards: Instant, but some banks might flag it. Good for smaller amounts.

- E-wallets (Skrill, Neteller): Fast and efficient, though they have their own fees.

- Cryptocurrency (USDT): Becoming hugely popular for speed and bypassing traditional banking hurdles. Deposit/withdrawal in minutes.

Pro Tip: Always use the same method for deposit and withdrawal where possible. It speeds up the process and reduces compliance checks. If you deposit via Skrill, plan to withdraw back to Skrill.

The SARB Allowances

Remember, you're still subject to South African Reserve Bank limits. The Single Discretionary Allowance (R1 million per year) covers things like travel and gifts. For investing/trading with an offshore-regulated broker (even if they have a local presence), you should technically use the Foreign Investment Allowance (R10 million per year), which requires a Tax Compliance Status PIN from SARS. Using an FSCA-regulated broker operating locally often falls within a grayer, simpler area, but it's wise to consult a tax professional. Your net trading profits are absolutely taxable as income.

“On a R1 million discretionary allowance, that's R30,000 gone before the money even leaves the country.”

Let's crystallize the difference. This table isn't just informative; it's the reason you choose one over the other.

| Feature | Nedbank (Netbank Forex) | FSCA-Regulated Forex Broker (e.g., IC Markets, Pepperstone) |

|---|---|---|

| Primary Purpose | Currency exchange for transactions, travel, business. | Speculative trading on currency price movements. |

| Your Role | Customer buying a product. | Trader taking a market position. |

| Cost Structure | Exchange rate margin (~2.5%) + fixed fees. | Tight spread (e.g., 0.2 pips on EUR/USD) + small commission. |

| Cost Example on R100k | ~R2,500 - R3,000 (2.5-3%) | ~R20 - R150 (0.02% - 0.15%) depending on trade size & pair. |

| Platform | Online banking portal. | MetaTrader 4/5, cTrader, proprietary platforms. |

| use | None (you buy the full amount). | Up to 30:1 for retail clients (FSCA mandate). |

| Can You Short Sell? | No. You can only buy the currency you need. | Yes. You can profit from markets falling as easily as rising. |

| Regulator | SARB, FSCA (as a bank). | FSCA (as a Financial Services Provider). |

| Best For | Sending money abroad, getting travel cash. | Actively speculating to generate profits from forex markets. |

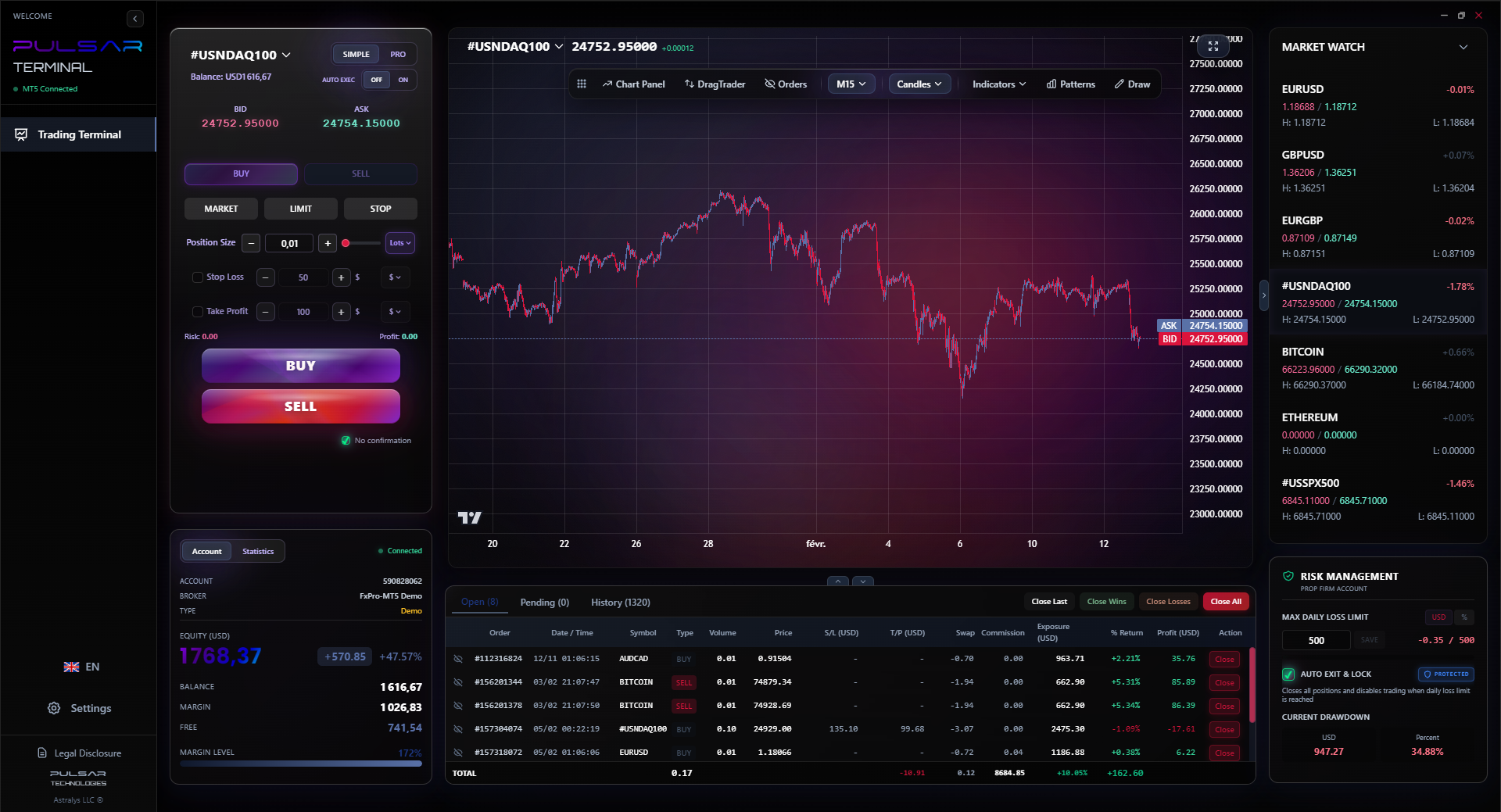

I made the mistake early in my career of using a bank's 'investment' platform that offered CFDs. The spreads were criminal - 10 pips on EUR/USD when the market was 2. I lost 8 pips the moment I entered the trade. I switched to a proper broker and never looked back. The tools alone - like proper charting and one-click trading - are worth it. Speaking of tools, managing trades on MT5 is where the game is won or lost. Setting multiple take-profits or moving stops to breakeven manually is a chore. This is where a good trading terminal becomes force multiplication.

[Pulsar Terminal promo slot context line: "Managing complex trades on MT5 is where a tool like Pulsar Terminal saves you from yourself, automating partial closures and trailing stops."]

💡 Winston'ın İpucu

A ZAR account with a local broker isn't just convenient. It's a strategic tax and cost-saving move. It turns forex friction from a 3% nightmare into a 0.1% afterthought.

Managing complex trades on MT5 is where a tool like Pulsar Terminal saves you from yourself, automating partial closures and trailing stops.

Pulsar Terminal

Hepsi bir arada MT5 aracı: sürükle-bırak emirler, çoklu TP/SL, trailing stop, grid trading, Volume Profile ve prop firm koruması. Her gün 1.000'den fazla trader tarafından kullanılıyor.

“Your first R10,000 in trading isn't capital. It's tuition.”

So you understand the difference now. If you want to trade, here's your roadmap, stripped of nonsense.

- Education Before Deposit: Don't put a cent in yet. Learn what a pip definition is, understand use, and grasp basic swing trading or scalping strategy concepts. Paper trade for at least three months.

- Choose an FSCA Broker: Pick from established names. I have experience with IC Markets for raw spreads and Pepperstone for their Razor account. Do your own research. Open a demo account first.

- Start Small, Think Big: Deposit an amount you can afford to lose completely - your 'tuition fee.' Use a position size calculator religiously. Risk 1-2% of your account per trade, no more. On a R10,000 account, that's R100-R200 risk per trade.

- Master One Pair & One Strategy: Don't jump from EUR/USD to Gold to USD/ZAR. Pick one major pair like EUR/USD guide or XAU/USD guide and learn its personality. Use one or two indicators like the RSI indicator or MACD indicator properly, not 10 badly.

- Keep a Journal: This is non-negotiable. Write down every trade: entry, exit, why you took it, your emotion. My journal from 2015 shows I lost 14 trades in a row trying to catch tops and bottoms. It was the best education I never paid for.

Your bank's netbank forex service has its place - for life admin. But for building capital, for taking control of your financial future through speculation, you need the right tool for the job. That tool is a regulated broker with a professional trading platform, not a banking app designed to sell you currency at a markup.

FAQ

Q1Can I trade forex directly through my Nedbank online banking?

No. Nedbank's netbank forex service is for currency exchange and international payments, not for speculative trading on price movements. You cannot open leveraged long/short positions, use MT4/5, or trade with the tight spreads of the interbank market through their retail banking platform.

Q2Is it legal for South Africans to use international forex brokers?

Yes, it is legal. However, it is significantly safer and simpler to use a broker that is regulated by the South African FSCA. If you use an offshore broker, the FSCA cannot help you if there's a dispute, and your South African bank may block the transactions due to exchange control regulations.

Q3What is the cheapest way to fund a forex trading account in South Africa?

Using a local EFT or payment method like Ozow to an FSCA-regulated broker that holds a local ZAR bank account. This is usually free and fast. Funding a USD account with an offshore broker via international wire transfer will incur your bank's forex margin and fees, making it expensive.

Q4Do I pay tax on my forex trading profits in South Africa?

Yes. Profits from forex trading are considered income and are subject to normal income tax in South Africa. You must declare them to SARS. Keep careful records of all your trades, statements, and deposits/withdrawals.

Q5Why are the spreads on USD/ZAR so much higher than on EUR/USD?

USD/ZAR is an exotic currency pair with lower liquidity and higher volatility compared to major pairs like EUR/USD. This results in wider spreads (e.g., 5 pips vs. 0.2 pips). The spread compensates the broker/market maker for the higher risk of facilitating trades in a less liquid market.

Q6What's the single biggest mistake new SA traders make with 'netbank forex'?

Thinking the exchange rate they see on their bank's app is the 'market rate' they can trade at. The bank's rate includes a large profit margin (2.5%+). Using that as a reference for trading decisions will guarantee losses. Always look at the live bid/ask spread on a professional trading platform for the true market price.

Prof. Winston'ın Dersi

Önemli Noktalar:

- ✓Bank forex margins are ~2.5%, broker trading costs are ~0.02%.

- ✓Use only FSCA-regulated brokers for safety & easy ZAR deposits.

- ✓Never trade without a position size calculator.

- ✓Taxable income includes all your forex trading profits.

Bu makale ne kadar faydalıydı?

Bir yıldıza tıklayın

Haftalık Trading Analizleri

Ücretsiz haftalık analiz ve stratejiler. Spam yok.

Yazar hakkında

David van der Merwe

Gelişen Piyasalar Yatırımcısı

Johannesburg merkezli, gelişmekte olan piyasa dövizlerinde 11 yıllık deneyime sahip trader. ZAR pariteleri, FSCA düzenlemeli ticaret ve Güney Afrika piyasa analizi uzmanı.

Yorumlar

Risk Uyarısı

Finansal araçlarla işlem yapmak önemli riskler taşır ve tüm yatırımcılar için uygun olmayabilir. Geçmiş performans gelecekteki sonuçları garanti etmez. Bu içerik yalnızca eğitim amaçlıdır ve yatırım tavsiyesi olarak değerlendirilmemelidir. İşlem yapmadan önce her zaman kendi araştırmanızı yapın.

Bunları da beğenebilirsiniz

Cara Trading Forex Sukses: 7 Prinsip dari Trader Profesional

Cara trading forex sukses dengan 7 prinsip trader pro: manajemen modal, disiplin, journal trading, backtest. Data nyata, bukan janji profit palsu.

Jam Trading Forex Terbaik untuk Trader Indonesia: Panduan Lengkap dengan Tabel Waktu

Panduan jam trading forex untuk trader Indonesia. Tabel 4 sesi dunia, jam emas 20:00-00:00, sesi mana yang harus dihindari. Data akurat + tips dari trader berpengalaman.

Top 5 Sàn Forex Uy Tín Nhất 2026: Review Jujur dari Trader Indonesia

Top 5 sàn forex uy tín 2026 untuk trader Indonesia. Review jujur: spread, deposit, withdraw, dukungan lokal. Exness, XM, IC Markets & lebih.

Pulsar Terminal'ı Edinin

Tüm bu hesaplayıcılar MT5 hesabınızdan gerçek zamanlı verilerle Pulsar Terminal'e entegredir.

Pulsar Terminal'ı Edinin