It was late February 2026, and a client's WhatsApp message popped up on my screen: 'My FNB card just got declined in London.

David van der Merwe

Emerging Markets Trader ·  South Africa

South Africa

☕ 10 min read

What you'll learn:

- 1What FNB Forex Actually Is (And What It Isn't)

- 2The Real Costs: Where FNB Makes Its Money

- 3The 'Forex Block' of 2026: A Game Changer for Many

- 4FNB vs. Real Forex Brokers: A Trader's Comparison

- 5FNB Global Trader: The Offshore Investment Angle

- 6Smart Alternatives for South African Traders

- 7When You *Should* Use FNB Forex (The Right Tool)

- 8The Final Verdict for 2026

It was late February 2026, and a client's WhatsApp message popped up on my screen: 'My FNB card just got declined in London. What the hell?' That was my first real-world encounter with FNB's now-infamous 'Forex Block' for foreign nationals. While that's a specific headache, it highlights a broader truth most South African traders need to hear: FNB Forex and active currency trading are two completely different beasts. I've watched too many new traders confuse a bank's currency services with a broker's trading platform, and it's a costly mistake. Let's strip away the marketing and look at what FNB Forex actually is, what it costs, and where you should really be putting your trading capital.

First, let's kill the biggest misconception right now. FNB Forex is not a leveraged forex broker. You are not going to log into their online banking and start scalping EUR/USD with 30:1 use. Thinking of it that way will set you up for failure and confusion.

What FNB provides is a foreign exchange and international payments service. It's for moving money across borders, hedging business exposure, or converting your Rands into Dollars for a holiday or an offshore investment. They act as the counterparty to your currency conversion. You want USD, they sell it to you at their rate. End of story.

Their services - spot transactions, forwards, options - are classic corporate treasury tools. For the average person, it's the channel you use to pay for an overseas course or receive freelance income from abroad. The platform is your familiar online banking or the FNB app. It's integrated, secure, and convenient for its intended purpose: moving value, not speculating on price movements.

If your goal is active trading - capturing small price fluctuations in currency pairs for profit - you need a dedicated, FSCA-licensed CFD broker like Exness or IC Markets. That's a different universe with different tools, risks, and fee structures. Mixing the two is like using a cargo ship for a speedboat race.

Banks don't do anything for free, and forex is a major profit center. The fees aren't always obvious, buried in the exchange rate itself. Here’s the breakdown that matters.

The Transfer Fees

These are the visible charges. Sending money overseas via FNB online will cost you either a flat fee (around R100-200 for smaller amounts) or a 0.55% commission for larger sums, with minimums and maximums. There's often an extra R130 'handling' fee if the payment is in ZAR. Receiving money costs similarly. It adds up, but it's predictable.

The Hidden Killer: The Exchange Rate Margin

This is the real bite. FNB doesn't give you the pure interbank rate you see on TradingView. They add a margin, typically between 2% and 4.5%. Let's make this painfully clear with a real number.

Example: On a day when the real EUR/ZAR rate is 20.0000, FNB might quote you a rate of 20.4000 to buy Euros (a 2% margin). On a R100,000 conversion, you're paying R2,000 extra, hidden in the worse rate. That's your true cost, far exceeding the stated transfer fee.

For major currencies like USD, GBP, and EUR, the margin tends to be on the lower end of that range. For exotic currencies, it widens. The only 'free' conversions are between ZAR and currencies pegged to it, like the Namibian Dollar.

There are some perks. The eBucks rewards can claw back up to 50% of the transaction charges, which is nice for regular users. And transfers between your own FNB ZAR and foreign currency accounts are free, which is useful if you maintain a USD balance for overseas expenses.

💡 Winston's Tip

A bank's 'competitive rate' still has a 2-4% margin baked in. On a R50k conversion, you're giving up R1,000 before you even start. That's not a trading cost, it's a convenience fee.

“The hidden killer is the exchange rate margin. On a R100,000 conversion, you could be paying R2,000 extra without seeing a separate fee.”

This is the big, recent development that's causing real pain. From around February 2026, FNB reportedly tightened controls on international transactions for certain customers, particularly foreign nationals.

If you're a foreign national in SA without a business permit, or you're freelancing from a personal account, you might find your card declined overseas, your PayPal withdrawals blocked, and online international purchases restricted. The message is clear: to move money out, you need a clear link to a business permit or a South African spouse/PR holder who can fund the account.

Warning: This isn't just an FNB policy quirk. It reflects intense pressure from the South African Reserve Bank (SARB) on exchange controls. If you're a trader relying on moving funds internationally - say, to fund an offshore broker account - this adds a significant layer of complexity. Your banking channel could suddenly become unreliable.

For South African citizens, the standard allowances apply: your R1 million Single Discretionary Allowance and up to R10 million Foreign Investment Allowance per year. But the 'Forex Block' shows the environment is getting stricter. Always keep your FICA documents updated and be prepared to explain the source and purpose of funds moving in and out. This regulatory mood makes the simplicity of a local, FSCA-licensed broker more attractive for trading activities.

To hammer the point home, let's put them side-by-side. This table isn't about which is better; it's about which tool is right for the job.

| Feature | FNB Forex | FSCA-Licensed Broker (e.g., Pepperstone) |

|---|---|---|

| Primary Purpose | Currency Exchange & International Payments | Speculative Trading on Price Movements |

| use | None (1:1) | Up to 30:1 for retail (FSCA limit) |

| Platform | Online Banking / FNB App | MT4, MT5, cTrader, Proprietary Platforms |

| Pricing | Exchange Rate Margin (2-4.5%) + Fees | Bid/Ask Spread + Possible Commission |

| Order Types | Market Orders for Transfers | Limits, Stops, Trailing Stops, OCO Orders |

| Charting & Analysis | Basic rate charts | Advanced charts, dozens of indicators, drawing tools |

| Instrument | The physical currency | CFDs on currency pairs, indices, commodities |

| Profit Mechanism | Saving on conversion costs / Hedging | Capital appreciation from price moves |

See the difference? Using FNB to trade is like trying to bake a cake with a screwdriver. The broker's platform is built for the analysis and execution speed trading demands. For example, trying to implement a basic scalping strategy through your FNB app is impossible. You can't set a 5-pip stop loss. You can't use the MACD indicator to time your entry. You're just buying currency at a marked-up price.

I learned this the awkward way early on. I tried to 'trade' by anticipating a stronger USD for an upcoming transfer. I converted a chunk of ZAR early. The USD then proceeded to tank. I was stuck with it, having locked in a terrible rate with FNB's margin baked in. My 'trade' was a loss the second I clicked confirm, with no way to exit. At a broker, I'd have had a stop-loss order to limit the damage.

💡 Winston's Tip

The 2026 'Forex Block' is a stark reminder: your banking channel is for life admin. Your trading platform is for speculation. Never mix the two. Keep separate accounts for clarity and to avoid regulatory headaches.

“Using FNB to trade is like trying to bake a cake with a screwdriver.”

This is FNB's offering that gets closer to actual trading. FNB Global Trader is a platform for buying and holding offshore assets - stocks, ETFs, etc. - not for trading forex CFDs. It's for longer-term investment.

They provide research, real-time data, and basic order types like stop-losses on equity positions. The security is solid (encryption, 2FA), and it's a regulated, integrated way for South Africans to use their foreign investment allowance.

But again, context is key. It's not a substitute for an active forex trading account. The costs are different (brokerage fees on share purchases), the execution speed is geared for investing, not intraday trading, and you can't apply use to forex pairs. It solves the problem of 'how do I invest offshore easily?' It does not solve the problem of 'how do I swing trade the AUD/NZD daily chart?'

For pure forex traders, even those with a swing trading horizon, the tighter spreads and advanced order management of a dedicated broker are non-negotiable. Trying to manage complex trade logistics - like scaling out with multiple take-profit levels - through a bank investment platform is clunky at best.

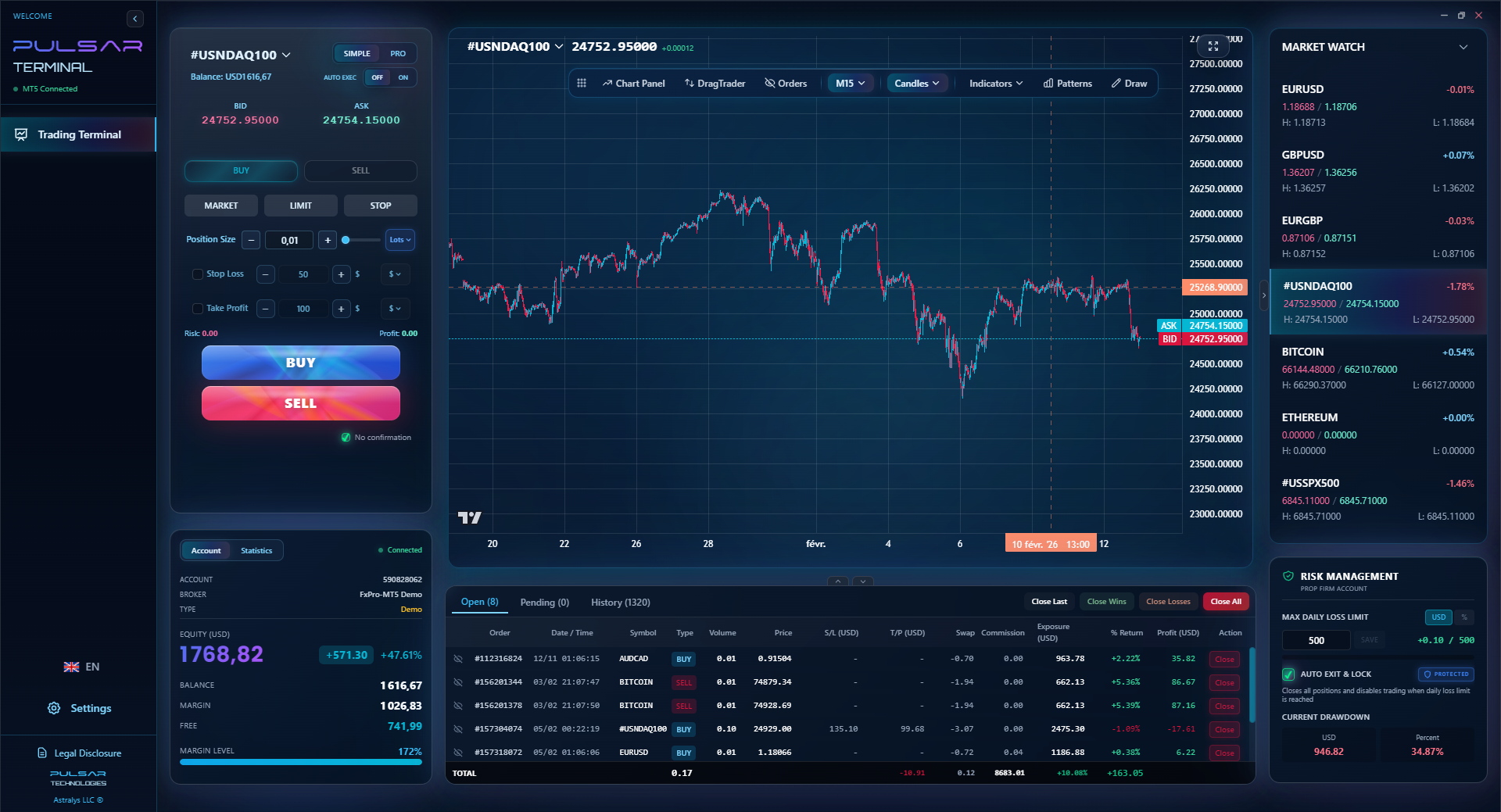

Managing complex trades with multiple take-profit levels is clunky on bank platforms, but tools like Pulsar Terminal make it drag-and-drop simple on MT5.

Pulsar Terminal

The all-in-one MT5 companion: drag-and-drop orders, multi-TP/SL, trailing stop, grid trading, Volume Profile, and prop firm protection. Used by 1,000+ traders daily.

So, if FNB Forex isn't for active trading, what is? Your best bets are right here at home.

- Local, FSCA-Licensed Brokers: This is the gold standard. Brokers like XM or IC Markets have local entities regulated by the FSCA. Your funds are held in segregated accounts in South Africa. Deposits and withdrawals are in ZAR via EFT, which is fast and avoids international wire fees. You get the full suite of trading tools, proper use (capped at 30:1 for retail), and spreads that are a fraction of a bank's margin. A typical spread on EUR/USD might be 0.1 pips versus FNB's effective 20,000-pip margin.

- International Brokers with Local Presence: Some global brokers accept South African clients smoothly. You'll fund in ZAR, but your trading account might be denominated in USD. This is fine, but be aware of the conversion cost when you deposit and withdraw.

- The Funding Workflow: Here’s a practical setup: Use your FNB (or any local bank) account for ZAR EFTs to your chosen FSCA broker. Do all your trading on the broker's platform (MT5, etc.). When you profit, withdraw back to your SA bank account. This keeps 95% of your activity in the efficient trading environment and only touches the banking system for in/out transfers.

I keep a separate, low-fee bank account just for broker transfers to keep things clean. It also makes tax time less of a nightmare. Remember, every time you involve an international wire, you're inviting FNB's fees and margins, and potentially, scrutiny under exchange control.

“If your decision is based on a chart, use a broker. If it's based on an invoice, use a bank.”

After all this, it sounds like I'm burying FNB Forex. I'm not. It's an excellent tool - when used for its intended purpose. Here’s when it makes perfect sense:

- You need physical foreign currency for travel or to pay an overseas invoice for your business.

- You're a business hedging currency risk. Setting up a forward contract through FNB to lock in a USD/ZAR rate for a future import payment is prudent financial management.

- You're receiving foreign income (e.g., from Upwork) and need to convert it to ZAR to live on.

- You're making a once-off, large offshore investment via a platform like Global Trader and want the integrated, secure channel.

- You're using your foreign investment allowance to move money to an overseas bank account you control.

In all these cases, you are not 'trading.' You are transacting. You are using banking infrastructure to move value from one place or form to another. The cost, while not cheap, is the price of that secure, regulated service. Comparing that cost to a broker's 0.6-pip spread is comparing apples to orbital rockets.

My rule of thumb: If your decision is based on an analysis of a chart, use a broker. If your decision is based on an invoice, a travel itinerary, or a long-term investment plan, a bank like FNB is the appropriate tool.

💡 Winston's Tip

Your first tool for risk management isn't a stop-loss; it's choosing the right platform. Trying to trade on a bank platform guarantees you'll have no effective risk controls. Start with the right foundation.

Look, FNB is a great bank. They've won 'Best Foreign Exchange Provider' awards for years, and for corporate services, they're the best in the country. But as a trader, you need surgical precision.

FNB Forex is a broadsword - heavy, effective for big, simple jobs. Active forex trading requires a scalpel. The 2026 'Forex Block' situation just reinforces that banks and regulators view capital movement differently from trading speculation.

Don't try to force one to do the other's job. Use FNB for what it's good at: moving your money securely across borders, converting currency for real-world needs, and managing your core banking. Then, take a portion of your risk capital and put it with a specialist broker where you can actually trade. Learn proper position sizing, manage your margin call risk, and use the right tools.

That separation of concerns - banking here, trading there - is what keeps you solvent, sane, and on the right side of the regulators. It’s the single biggest piece of operational advice I can give any South African starting out. Get that foundation right, and then you can worry about nailing your EUR/USD entries.

FAQ

Q1Can I trade forex with use on FNB?

No, absolutely not. FNB Forex is a currency exchange and international payment service. You cannot open a leveraged CFD trading account to speculate on forex pairs through FNB's online banking. For that, you need an FSCA-licensed broker like IC Markets or Exness.

Q2What is the 'FNB Forex Block' I keep hearing about?

In early 2026, FNB reportedly tightened exchange control compliance, restricting international transactions for certain clients, particularly foreign nationals without specific permits. This can lead to declined overseas card payments, blocked PayPal withdrawals, and restricted online international purchases. It highlights the strict regulatory environment for moving money out of South Africa.

Q3Are FNB's forex rates good?

For a bank, they're competitive. But 'good' is relative. They add a margin of 2-4.5% to the interbank rate. For a R100,000 conversion, that's an extra R2,000-R4,500 cost. For a one-off holiday payment, it's acceptable convenience. For frequent trading, it's prohibitively expensive compared to a broker's spread of a few cents.

Q4Should I use FNB Global Trader to trade?

Only if you mean 'invest.' Global Trader is for buying and holding offshore shares and ETFs. It is not a platform for active forex or CFD trading. It lacks the advanced charts, order types, and use necessary for short-term trading strategies.

Q5How do I fund an international forex broker from South Africa?

The easiest way is to use a locally regulated broker that accepts ZAR EFTs. You transfer Rands from your FNB (or any SA) account directly to the broker's South African bank account. This avoids international wire fees and FNB's exchange margin. The broker then converts it to your trading account currency (often USD) at a much better rate.

Q6Is it legal to trade forex in South Africa?

Yes, it is completely legal. The Financial Sector Conduct Authority (FSCA) regulates the industry. You must use an FSCA-licensed broker, which provides important protections like client fund segregation. Retail use is capped at 30:1.

Q7What's the single biggest mistake South Africans make with FNB and forex?

Confusing currency conversion with currency trading. They see 'forex' at their bank and think it's the same as the trading they see online. This leads to using the wrong tool, paying enormous hidden costs, and having no ability to manage risk with stop-losses. They're two separate activities requiring separate platforms.

Prof. Winston's Lesson

Key Takeaways:

- ✓FNB Forex is for payments, not leveraged trading.

- ✓The real cost is a 2-4.5% margin on the exchange rate.

- ✓The 2026 'Forex Block' shows increasing regulatory scrutiny.

- ✓Use local FSCA brokers for trading; use banks for banking.

- ✓Separate your trading and banking accounts completely.

How useful was this article?

Click a star to rate

Weekly Trading Insights

Free weekly analysis & strategies. No spam.

About the Author

David van der Merwe

Emerging Markets Trader

Johannesburg-based trader with 11 years in emerging market currencies. Specializes in ZAR pairs, FSCA-regulated trading, and South African market analysis.

Comments

Risk Disclaimer

Trading financial instruments carries significant risk and may not be suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always conduct your own research before trading.

You Might Also Like

Cara Trading Forex Sukses: 7 Prinsip dari Trader Profesional

Cara trading forex sukses dengan 7 prinsip trader pro: manajemen modal, disiplin, journal trading, backtest. Data nyata, bukan janji profit palsu.

Jam Trading Forex Terbaik untuk Trader Indonesia: Panduan Lengkap dengan Tabel Waktu

Panduan jam trading forex untuk trader Indonesia. Tabel 4 sesi dunia, jam emas 20:00-00:00, sesi mana yang harus dihindari. Data akurat + tips dari trader berpengalaman.

Top 5 Sàn Forex Uy Tín Nhất 2026: Review Jujur dari Trader Indonesia

Top 5 sàn forex uy tín 2026 untuk trader Indonesia. Review jujur: spread, deposit, withdraw, dukungan lokal. Exness, XM, IC Markets & lebih.

Get Pulsar Terminal

All these calculators are built into Pulsar Terminal with real-time data from your MT5 account. One-click position sizing, automatic risk management, and instant calculations.

Get Pulsar Terminal