Slippage

SLIP-ijsince Early 1990s interbank forex eraSlippage — when your trade fills at a different price than you clicked — like ordering a coffee for $5 but getting charged $5.03 at the register.

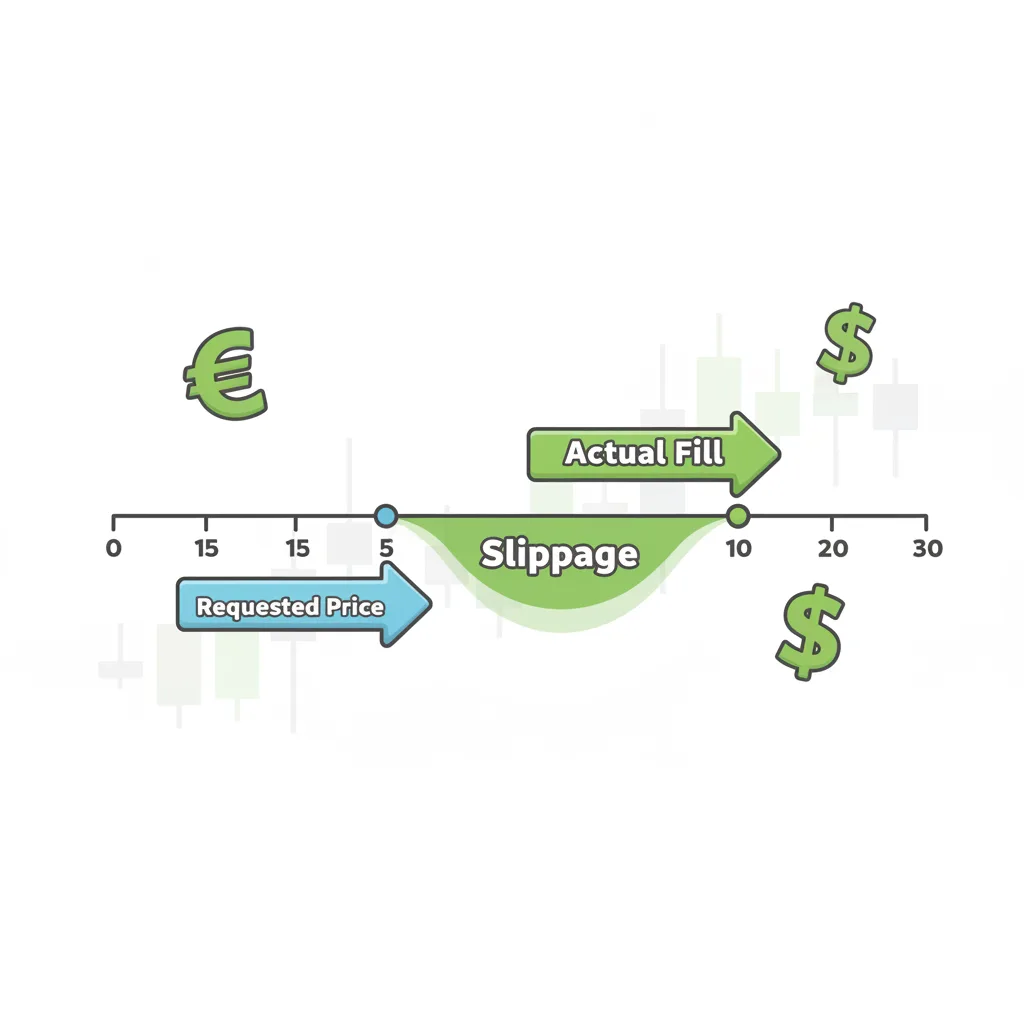

§1So what IS slippage, really?

Okay, picture this: you're at a busy coffee shop during the morning rush. You order your latte for $5.00, but by the time the cashier rings it up, the price has jumped to $5.03 because demand just spiked. That's slippage in trading — the difference between the price you asked for and the price you actually got. It's that little gap between clicking 'buy' and your broker saying 'done!' In forex and CFD trading, slippage happens when prices move faster than your order can be filled. Sometimes it works in your favor (positive slippage — getting that latte for $4.97 instead!), but more often it's negative. I've seen traders blow accounts over this during news events, so trust me, you want to understand this one. Think of it like trying to catch a specific subway car as it's pulling out of the station — you might grab the handle you aimed for, or you might end up a few doors down.

§2The math (don't run away — it's simpler than it looks!)

I know, I know — formulas make your eyes glaze over. But stick with me for 30 seconds, and you'll get it. The basic slippage formula is: Slippage (in pips) = (Execution Price - Requested Price) × (1 / Pip Size). See? Not so scary! For most pairs like EUR/USD, a pip is 0.0001. So if you wanted to buy at 1.2000 but got filled at 1.2003, you'd do: (1.2003 - 1.2000) × (1 / 0.0001) = 0.0003 / 0.0001 = 3 pips of slippage. That's it! The trickiest part is remembering that JPY pairs use 0.01 instead of 0.0001 — but we'll get to those weirdos in a minute. The key takeaway? This formula just measures how far the price 'slipped' from your target.

§3Here's how it plays out in real life

Let's walk through what actually happens when slippage occurs. Say you're trading EUR/USD and you place a market buy order at 1.1000. You click, your broker sends the order... but in that split second, some economic news drops and the price jumps to 1.1003. Your order gets filled at that new price — boom, 3 pips of negative slippage. Now imagine the opposite: you place a buy limit order at 1.1965 for GBP/USD, hoping to catch a dip. The market tanks faster than expected, and your order fills at 1.1962 — that's 3 pips of positive slippage! You just saved money without even trying. The mechanism is simple: if prices move between your order and its execution, you get slippage. During calm markets, this might be just 1-3 pipettes (0.1-0.3 pips). During volatility? Buckle up — it can hit 10-15 pips or more.

§4Special cases (yes, JPY is being weird again)

Alright, time for the exceptions nobody warns you about. First up: JPY pairs. While most currency pairs use four decimal places (like EUR/USD at 1.1000), JPY pairs typically use two (USD/JPY at 155.00). This means their pip size is 0.01 instead of 0.0001. So when you're setting slippage tolerance on MT4/MT5, you need to adjust your numbers accordingly. Then there's Guaranteed Stop-Loss Orders (GSLOs) — these magical orders eliminate slippage risk entirely. Your broker promises to close your trade at exactly your specified price, even if the market gaps. The catch? They usually charge a premium if it triggers. And don't get me started on exotic pairs or trading during holidays — with thin liquidity, slippage becomes as common as pigeons in a city park.

§5Three examples that'll make it click

Let's look at three real scenarios you might face:

| Scenario | Pair | Requested Price | Actual Price | Slippage | Outcome |

|---|---|---|---|---|---|

| Market Buy during news | EUR/USD | 1.1000 | 1.1003 | 3 pips negative | Paid more than expected |

| Limit Buy during drop | GBP/USD | 1.1965 | 1.1962 | 3 pips positive | Got a better deal |

| Stop-loss during gap | EUR/USD | 1.1030 (SL) | 1.1020 | 10 pips negative | Lost extra 10 pips |

See how that works? In the first example, you wanted to buy at 1.1000 but got 1.1003 — that's like aiming for the front row at a concert and ending up three rows back. The second example is the happy accident: you wanted 1.1965 but got 1.1962. The third? That's the nightmare scenario where your stop-loss gets triggered way past where you set it. My first year trading, I lost $200 on a single trade from exactly this kind of slippage during a Fed announcement.

§6Where this thing even came from

Slippage isn't some newfangled concept — it's been around as long as markets have had fluctuating prices. But traders really started paying attention after some legendary market meltdowns. The most famous? January 2015, when the Swiss National Bank unexpectedly removed the EUR/CHF peg. Overnight, EUR/CHF and USD/CHF dropped like rocks in a pond. USD/CHF fell 2780 pips in just 30 minutes — yes, you read that right. Stop-loss orders that traders thought were safe executed at dramatically worse prices. Some accounts got wiped out completely. That event taught the trading world that slippage isn't just a minor inconvenience — it can be a portfolio-wrecker. Since then, brokers have developed tools like GSLOs and better execution models, but the fundamental reality remains: when markets move fast, prices can slip.

§7Key takeaways

- Slippage is the difference between your requested price and actual fill — it can be positive (good) or negative (bad).

- During major news events, slippage can spike to 10-15+ pips, even on major pairs like EUR/USD.

- Use limit orders and avoid high-volatility periods if you want to minimize slippage risk.

- Always check your slippage tolerance settings on MT4/MT5 — especially with 5-digit brokers where '30' might mean 3 pips.

§8Frequently asked questions

QWhat causes slippage in Forex?

QHow can I avoid or minimize slippage?

QIs slippage always a bad thing?

QHow do I set max slippage in MT4/MT5?

QWhat is positive slippage?

§See also

§References

- Swiss National Bank Removes EUR/CHF Cap — Financial Market Analysis

- MetaTrader Platform Documentation — MetaQuotes Software